While the act of moving stablecoins might appear straightforward and instantaneous on the surface, the underlying reality is often far more complex. Beneath the hood, what seems like a simple transfer is frequently a multi-step, intricate transaction, meticulously routed across disparate chains and liquidity pools. Ryne Saxe, CEO of Eco, a company specializing in stablecoin infrastructure, highlighted this critical issue to Cointelegraph, stating, “It’s a very special case of a foreign exchange market onchain, and that leads to bad user experience, with unexpected slippage, transaction reversion and unfamiliar information when moving your dollar from point A to point B.” This fragmented architecture not only introduces operational complexities but also elevates the risk profile for users attempting to navigate the burgeoning stablecoin landscape.

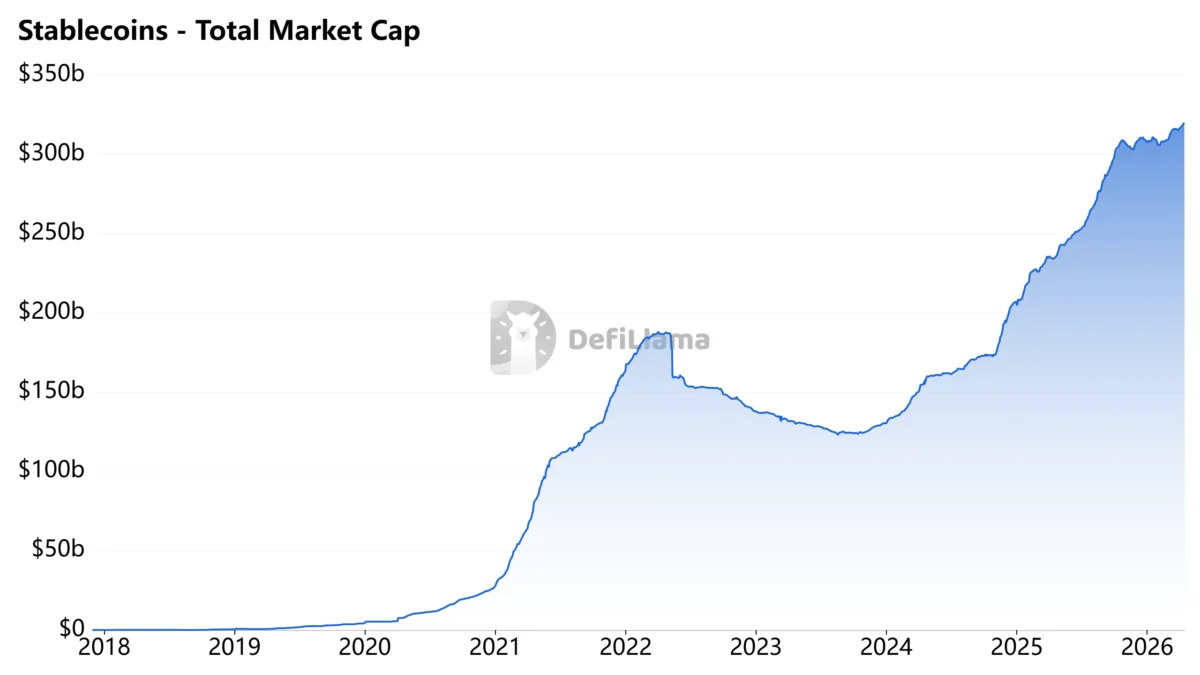

The stablecoin market has witnessed phenomenal growth, with its total capitalization now soaring above $320 billion. This expansion is largely spearheaded by industry giants such as Tether’s USDt (USDT) and Circle’s USDC (USDC). These digital assets have become indispensable rails for value transfer within the crypto economy, serving as critical intermediaries for trading, lending, and a myriad of other financial activities. However, as the market matures and attracts a growing influx of institutional players and large-volume traders, the challenge of efficiently moving substantial sums of stablecoins without incurring significant costs or disruptions becomes progressively more difficult. The sheer volume of these transactions exacerbates the underlying issues of liquidity fragmentation, making clean and predictable execution a formidable task.

The notion that stablecoins are inherently fungible, much like physical dollars, is proving to be a misconception within the digital realm. A stablecoin, even if meticulously pegged to the U.S. dollar—or indeed, other G7 fiat currencies—does not trade as a singular, unified asset across the entire crypto ecosystem. Instead, its liquidity is fractured across a diverse array of issuers, distributed across numerous blockchain networks, and spread thin over countless decentralized finance (DeFi) venues. Each of these distinct segments possesses its own unique liquidity depth, pricing mechanisms, and specific access conditions. Saxe emphasized this point, noting, “Stablecoins, between them, aren’t very fungible. The different profiles between those markets mean pricing and moving stablecoins seamlessly and efficiently across them is actually a hard problem that people take for granted.”

In practical terms, a dollar-pegged stablecoin residing on one blockchain might not hold the exact same value or liquidity profile as the "same" asset on another chain. This divergence stems from several factors, including differences in the underlying collateral backing mechanisms, varying market access points, and disparate liquidity depths within specific pools. Such variations inevitably create pricing gaps, which, while often negligible for smaller transactions in highly liquid markets, tend to widen dramatically when larger trade sizes are involved or when transactions are attempted in thinner, less liquid markets. The fundamental principle of fungibility, which dictates that units of an asset should be mutually interchangeable, is thus challenged in the stablecoin space.

Saxe further elaborated on this growing fragmentation, stating, “The more major DeFi markets focus on stablecoins, the more chains focus on stablecoins, the more stablecoin assets there are, the more fragmented. People think these are just dollars, but they’re actually not.” This increasing diversification, while promoting innovation, simultaneously complicates the very essence of stablecoin utility – predictable and efficient value transfer. The user experience suffers directly from this fragmentation. Unexpected slippage, where the executed price differs significantly from the expected price, can lead to financial losses. Transaction reversion, where a transaction fails after initial submission, wastes gas fees and time. Furthermore, the unfamiliar information required to navigate complex multi-chain, multi-pool routes presents a steep learning curve and operational overhead for even seasoned participants.

Empirical evidence supports these observations. A March report published by payments startup Borderless revealed that pricing divergence in stablecoins is heavily influenced by the source of liquidity. The report meticulously collected hourly buy and sell rates throughout February across 66 stablecoin-to-fiat corridors, encompassing 33 fiat currencies and operating across seven distinct blockchains. While the data generally indicated that USDC and USDT traded at near-identical prices in the majority of these corridors, with 91% of pairs falling within a narrow 10 basis point range, more significant discrepancies emerged at the provider level. Within the same corridor, pricing gaps could exceed hundreds of basis points, underscoring that the quality and efficiency of execution are highly dependent on a user’s access to optimal liquidity and their ability to route transactions intelligently across various venues. This highlights a crucial challenge: simply having a stablecoin doesn’t guarantee a uniform dollar equivalent; its value can fluctuate based on where and how it’s traded.

The current market structure of stablecoins bears a striking resemblance to traditional foreign exchange markets, where various dollar proxies (like different national currencies pegged to the USD) circulate across a network of disconnected markets, each with its own liquidity dynamics and pricing nuances. This analogy becomes particularly pertinent and visible when larger stablecoin movements are attempted across different blockchain networks. For institutions venturing into the digital asset space, stablecoins have rapidly become a cornerstone. They are widely utilized for a broad spectrum of activities, including high-volume trading, facilitating cross-border payments, and implementing on-chain treasury management strategies. Firms rely on these digital dollars to seamlessly move capital between diverse trading venues, efficiently settle complex trades, and actively pursue yield-generating opportunities across the vast and interconnected DeFi markets.

However, unlike retail users who typically transact smaller amounts, institutional players routinely need to move tens of millions of dollars at a time. For these large-scale operations, execution speed, predictability, and efficiency are paramount. The fragmented nature of stablecoin liquidity presents a significant constraint in such scenarios. Saxe elaborated on this, explaining, “If liquidity is spread out, trying to sell $10 million of one stablecoin and buy $10 million of another in a single step will move the market. What usually needs to happen is breaking that transaction into multiple branches, which may route differently and converge at the destination.” This fragmentation forces institutions to navigate a complex web of multiple chains, numerous issuers, and varied venues, each presenting distinct liquidity conditions. Attempting to move substantial sums can inadvertently shift prices, necessitating the splitting of trades into smaller, more manageable chunks, and introducing a degree of uncertainty into the overall execution process. Such complexity directly impacts the efficiency and cost-effectiveness of institutional participation in the digital asset economy.

The current state of stablecoin infrastructure is inadequate for the scale and sophistication required by institutional participants. Saxe underscored this, stating, “Right now, they don’t have the risk management, trust and infrastructure that they need to move or hold a lot of stablecoins at size onchain by default.” This highlights a critical gap in the market: while stablecoin supply has grown exponentially, the underlying plumbing to manage that supply efficiently for large-scale operations has not kept pace. Institutions require robust, reliable, and predictable systems that can minimize market impact, reduce slippage, and provide transparent execution. Without such infrastructure, the full potential of stablecoins as a foundational layer for institutional digital finance remains untapped.

Recognizing these critical gaps, various companies are now actively developing infrastructure solutions, albeit from different conceptual starting points regarding the core problem. Circle, for instance, is approaching stablecoins as the fundamental building blocks of an entirely new foreign exchange system. Their vision involves connecting multiple currencies, diverse liquidity providers, and various settlement layers through a shared, interoperable infrastructure, aiming to create a unified global network for digital currency exchange. In contrast, Eco, as articulated by Saxe, is focusing intensely on optimizing the routing and execution of stablecoin transactions, with the goal of aggregating and intelligently navigating liquidity across the inherently fragmented existing markets.

Both of these distinct approaches implicitly acknowledge the central challenge: stablecoins exist across a multitude of chains and are issued by various entities, but the crucial liquidity underpinning them remains distributed and uneven. Moving funds effectively necessitates interacting with this fragmented liquidity, which, as established, introduces pricing disparities, routing complexities, and inherent execution risks. Saxe articulated Eco’s perspective on this, stating, “Fragmentation creates more spread between prices, meaning worse execution in many cases. To solve that, you need to read across markets, see the full liquidity picture, even if it’s fragmented, and route across it.” This "full liquidity picture" approach aims to provide institutions with the visibility and tools to overcome the challenges posed by a dislocated market.

For institutional players, this pervasive complexity directly imposes limits on the amount of capital that can be efficiently and safely moved on-chain. As Saxe emphatically explained, stablecoin flows must achieve a far greater degree of predictability and reliability before institutions can cultivate the necessary risk management frameworks and establish the requisite trust to confidently move or hold substantial amounts of capital on-chain. This extends beyond mere technological solutions; it involves developing robust legal frameworks, enhancing regulatory clarity, and fostering a secure operational environment that mitigates various risks, including market risk, operational risk, and counterparty risk.

The broader implications of this fragmentation extend to the ongoing discussions around regulatory oversight. As jurisdictions like the EU (with MiCA) and the US grapple with stablecoin regulation, the fragmented nature of these assets presents unique challenges for supervision and ensuring financial stability. A unified regulatory approach is difficult when the asset itself lacks unified behavior across different ecosystems. Furthermore, the rise of Central Bank Digital Currencies (CBDCs) could either exacerbate or alleviate this fragmentation, depending on their design and interoperability with existing stablecoin ecosystems.

Ultimately, the journey of stablecoins from niche crypto assets to pivotal instruments in global finance is contingent on overcoming this inherent fragmentation. The focus must shift from simply increasing the supply of stablecoins to building the sophisticated, robust, and intelligent infrastructure required to manage their liquidity and facilitate seamless, predictable, and efficient movement, especially for institutional-scale operations. Only then can stablecoins truly fulfill their potential as a stable, reliable, and universally accessible digital dollar, transcending their current limitations as a collection of dislocated digital currencies.