Bitcoin’s (BTC) price action has been meticulously confined within a $10,000 corridor, specifically oscillating between the critical $60,000 and $70,000 thresholds, for the better part of the last two months. This persistent range-bound trading, a source of both frustration and strategic positioning for market participants, is not merely a random occurrence. Instead, it is the culmination of several interconnected market dynamics: the overwhelming influence of leverage-dominant futures trading, a conspicuous lack of robust spot market demand, and the continuous pressure exerted by short-term holders grappling with sustained losses. Together, these elements forge a delicate and volatile market structure where Bitcoin’s stability is less a function of organic capital inflows and more a precarious balance of futures positioning, explaining its current agitated equilibrium.

The Dominance of Derivatives: A Futures-Led Market

The primary driver dictating Bitcoin’s immediate price trajectory appears to be the derivatives market, particularly perpetual futures. According to analysis by Wintermute, a prominent crypto market maker, activity in the perpetual futures market continues to dwarf spot market participation across major exchanges. The perpetual-to-spot volume ratio has alarmingly escalated to 15 times (15X), a clear indicator that price discovery and direction are predominantly controlled by highly leveraged positions rather than genuine buying or selling pressure in the underlying asset.

This pronounced reliance on leverage creates a fragile ecosystem. When a market is so heavily skewed towards derivatives, it becomes highly susceptible to rapid price swings triggered by cascading liquidations, rather than fundamental shifts in supply and demand. The very nature of perpetual futures, which allow traders to speculate on price movements without owning the underlying asset, means that conviction can be fleeting.

Adding another layer to this derivatives-driven narrative are the funding rates – periodic payments exchanged between long and short traders in the perpetual futures market. These rates oscillate erratically, frequently flipping between positive and negative values without establishing a sustained directional bias. A consistently positive funding rate typically signals a bullish sentiment among futures traders, indicating a willingness to pay longs to maintain their positions. Conversely, a negative rate suggests bearish sentiment. The current oscillation, however, paints a picture of profound indecision and a lack of strong, collective conviction among futures traders. They are quick to open and close positions, adapting to minor price fluctuations rather than betting on a decisive trend.

Further underscoring this point, the volatility of these funding rates has compressed significantly, dropping to 2.9% from a healthier 5% range observed in 2025 (likely a typo, intended for 2024 or earlier). This compression signals that the amplitude of swing trades in futures positioning has diminished. While traders are still actively utilizing leverage, their bets are smaller, more cautious, and lack the assertive conviction typically seen during strong market trends. This implies a market populated by tactical, short-term players looking to scalp profits from minor movements, rather than strategic investors committing capital for a sustained rally or decline.

This confluence of factors — high perp-to-spot ratio, oscillating funding rates, and compressed funding rate volatility — points to a "coiling market structure." This analogy suggests that the market is like a spring being compressed, building up potential energy. However, unlike a spring that eventually snaps with force, the current coiling is characterized by indecisive, short-term leverage flows that remain the dominant force, preventing any significant release of that pent-up energy in either direction. The market is waiting for a catalyst, but its current structure makes it highly vulnerable to sudden, sharp moves once that catalyst appears, due to the inherent instability of leverage.

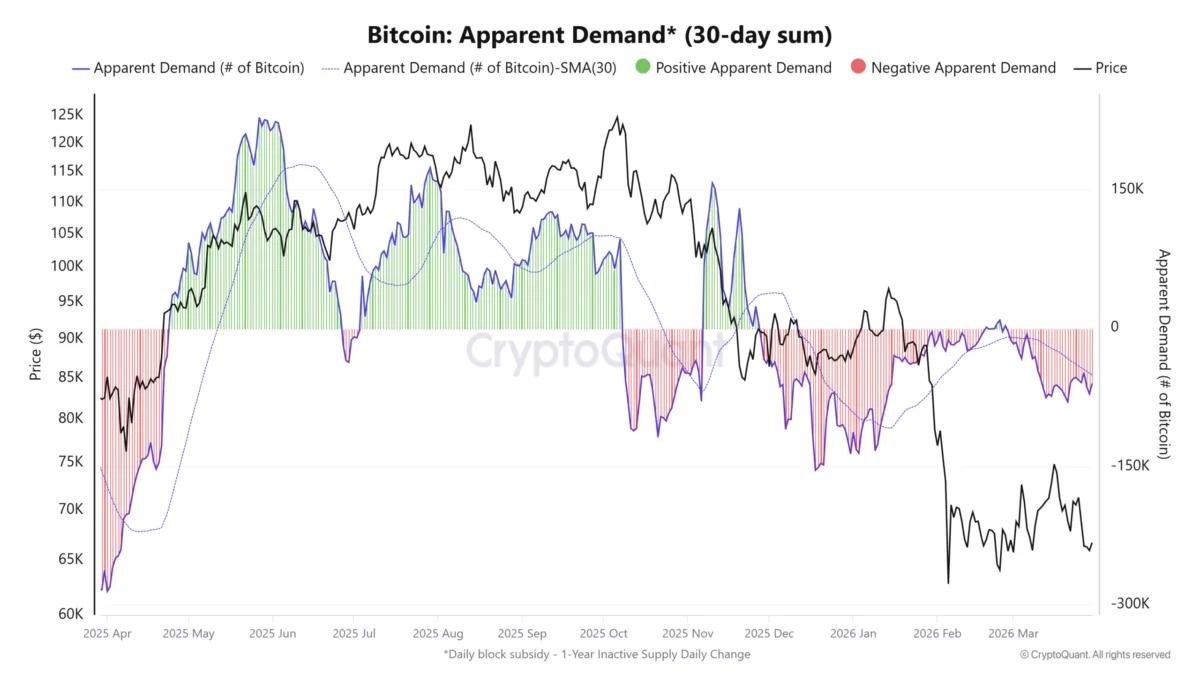

Anemic Spot Demand: The Missing Ingredient

While derivatives dictate the short-term dance, the underlying lack of genuine spot market demand is the fundamental weakness preventing Bitcoin from breaking out of its current range and establishing sustained rallies. True price stability and upward momentum ultimately depend on fresh capital inflows into the spot market, where investors actually buy and hold BTC.

On-chain metrics paint a stark picture of this demand deficit. According to CryptoQuant, the 30-day "apparent demand" metric currently sits at a concerning -60,000 BTC. This figure signifies that over the past month, more Bitcoin has moved out of exchanges than has been accumulated, indicating net selling or withdrawal rather than active buying. A healthy bull market is typically characterized by sustained positive apparent demand, reflecting accumulation and increasing investor interest.

Another critical barometer for future buying power is the inflow of stablecoins into spot exchanges. Stablecoins, such as USDT and USDC, often serve as a proxy for dry powder waiting to be deployed into crypto assets. Currently, the total stablecoin inflows into spot exchanges are hovering near $452 million. While this might seem substantial in isolation, it represents a level close to a two-year low. This metric is particularly concerning as it indicates a significant reduction in new capital entering the market with the intent to purchase Bitcoin or other cryptocurrencies. The initial euphoria surrounding the approval of spot Bitcoin ETFs in the U.S. earlier this year led to a surge in capital, but that enthusiasm appears to have waned, leaving a vacuum where fresh funds once flowed. This lack of new liquidity severely limits the potential for any sustained upward price movement.

Short-Term Holders Under Duress: A Cycle of Losses

Adding another layer of pressure to Bitcoin’s price action is the precarious position of short-term holders (STHs). These are investors who typically hold Bitcoin for less than 155 days and are often more susceptible to market fluctuations and emotional decision-making. Their collective psychology and behavior can significantly impact market trends.

The "realized price" for this cohort, which represents their average entry cost, is currently estimated to be around $85,800. With Bitcoin consistently trading far below this level, a substantial portion of recent buyers find themselves holding unrealized losses. This "underwater" status creates a powerful psychological barrier, as these holders are naturally inclined to sell their positions as soon as the price approaches their breakeven point, or even at a smaller loss, to mitigate further downside or simply to exit a losing trade.

Bitcoin researcher Axel Adler Jr. has highlighted two key metrics that vividly illustrate the persistent stress experienced by short-term holders. The first is the Short-Term Holder Spent Output Profit Ratio (SOPR). This metric tracks whether coins are being sold at a profit or a loss. A SOPR value below 1 indicates that, on average, STHs are selling their Bitcoin at a loss. Alarmingly, the STH SOPR has remained below 1.0 for over 110 consecutive days. This extended period of loss-taking is a clear sign of capitulation and fatigue among recent buyers, suggesting that many are simply giving up and exiting their positions even at a loss.

The second metric, the short-term holder realized price year-on-year (YOY), further corroborates this narrative. This metric has dropped to -5.35%, marking the first negative reading since the depths of the 2022 bear market. This is a critical indicator, as it confirms that the losses incurred by short-term holders are not merely fleeting corrections but have persisted over several months, mirroring the prolonged pain experienced during previous market downturns.

When a significant segment of the market, particularly the short-term speculative cohort, is consistently underwater, their behavior fundamentally alters market dynamics. The tendency to "sell into strength" – liquidating positions during minor rallies to cut losses or break even – creates a powerful overhead resistance. This constant selling pressure prevents any nascent upward momentum from gaining traction, effectively capping the price and limiting upside potential. This cycle of buying high, seeing the price drop, and then selling into any recovery reinforces the fragile market structure and keeps Bitcoin trapped within its current range.

The Halving’s Shadow and Macro Headwinds

The current market stagnation also occurs against the backdrop of the recently concluded Bitcoin Halving event in April. Historically, halvings, which reduce the supply of new Bitcoin, have been precursors to significant bull runs. However, the anticipated supply shock appears to be struggling to manifest its full price impact due to the demand-side weaknesses outlined. The market seems to be in a post-halving "digestion" phase, where the supply reduction is present, but the necessary buying pressure to absorb it and drive prices higher is absent.

Furthermore, broader macroeconomic factors cannot be ignored. Persistent inflation concerns, the Federal Reserve’s cautious stance on interest rate cuts, and geopolitical uncertainties continue to influence investor sentiment across all asset classes, including cryptocurrencies. Traditional financial markets remain volatile, and this general air of caution often translates into reduced appetite for riskier assets like Bitcoin, especially from larger institutional players who might be waiting for clearer macro signals before allocating substantial capital.

Breaking the Stalemate: What’s Needed for a Breakout?

For Bitcoin to finally break free from its $60,000-$70,000 straitjacket, a confluence of positive developments is required. The primary need is a resurgence of genuine spot market demand. This could come from renewed retail interest, significant institutional capital inflows (perhaps driven by a more favorable macroeconomic outlook or new compelling narratives), or a combination of both. A sustained period of positive apparent demand and increasing stablecoin inflows would signal a healthy return of buying pressure.

Secondly, the derivatives market needs to find a clearer directional bias. This could involve funding rates consistently turning positive, indicating strong bullish conviction, or a cleansing event through a sharp price correction that liquidates over-leveraged positions, paving the way for more organic growth.

Finally, the psychology of short-term holders needs to shift. This might entail a period of capitulation, where the weakest hands are flushed out, allowing for a healthier market base. Alternatively, a prolonged period of consolidation or a slow grind upwards could gradually bring STHs back into profit, reducing their selling pressure.

Conclusion

Bitcoin’s current entrapment within the $10,000 range is a complex interplay of leverage-driven trading, a palpable lack of spot market interest, and the persistent stress on short-term holders. The market’s reliance on derivatives for price stability creates an inherently fragile environment, susceptible to sudden swings but lacking the conviction for sustained trends. With limited fresh capital entering the spot market and a significant cohort of recent buyers underwater, the path of least resistance appears to be continued consolidation or even a further retest of lower support levels before any meaningful upward trajectory can be established. The "coiling spring" analogy perfectly captures the current state – a market building tension, awaiting a decisive catalyst, but one whose eventual release could be volatile in either direction. Until genuine spot demand returns and short-term holders find relief, Bitcoin may remain tethered to its current range, a testament to the intricate dynamics governing its highly speculative yet increasingly institutionalized market.