The White House’s Office of Information and Regulatory Affairs (OIRA) has concluded its pivotal review of a Department of Labor (DOL) proposal, marking a significant milestone that could fundamentally alter how fiduciaries overseeing 401(k) retirement plans evaluate and incorporate alternative assets, including crucial exposure to digital assets. This development signals a profound shift in federal policy, potentially opening the vast U.S. retirement market to cryptocurrencies and other non-traditional investments.

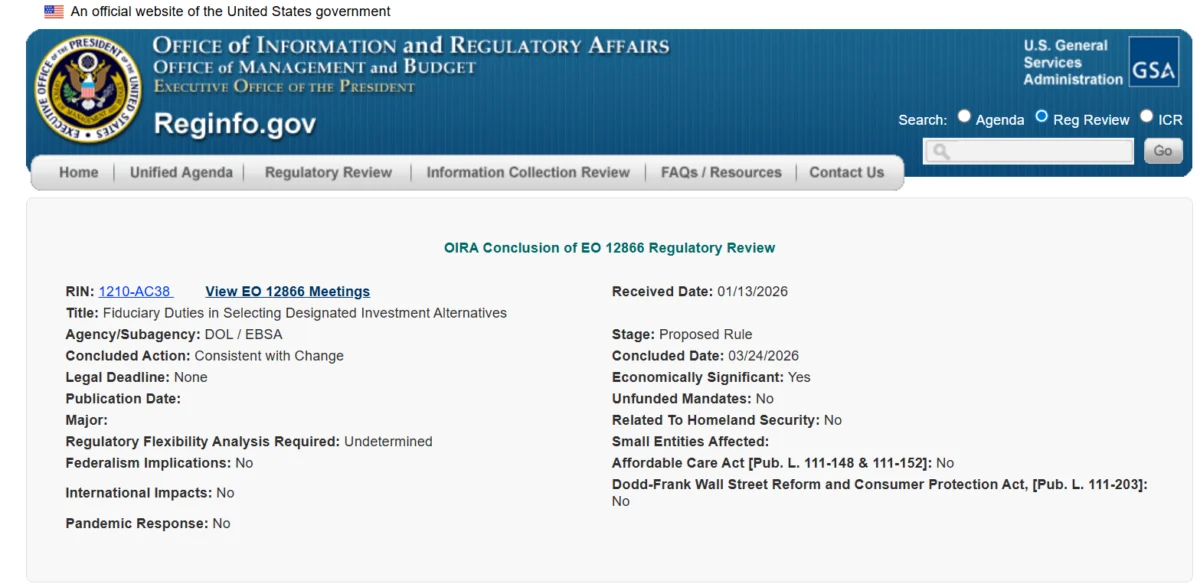

On March 24, the OIRA’s website confirmed the completion of its review, categorizing the action as "consistent with change" and designating the proposal as "economically significant." This classification underscores the projected widespread impact of the rule on the financial landscape and millions of American savers. The "consistent with change" designation typically implies that while some minor modifications may have been made during the interagency review process, the core intent and substance of the DOL’s original proposal remain intact. This outcome clears a crucial interagency hurdle, paving the way for the DOL to proceed with publishing the proposed rule. Following publication, a standard 60-day public comment period will commence, allowing stakeholders, financial institutions, industry experts, and the general public to submit feedback. This period is typically followed by careful consideration of comments, potential revisions to the rule, and ultimately, the issuance of a final, legally binding regulation.

This regulatory initiative stems directly from President Donald Trump’s executive order issued on August 7, 2025. This landmark order explicitly directed federal agencies to expand access to a broader range of alternative assets within 401(k) plans, with a particular focus on digital assets accessible through specified investment vehicles. The executive order mandated that the DOL reevaluate existing restrictions surrounding alternative assets in defined-contribution plans, specifically citing digital assets, private equity, and real estate. Furthermore, it called for enhanced inter-agency collaboration between the U.S. Treasury Department and the Securities and Exchange Commission (SEC) to support and facilitate the necessary rule changes, highlighting a concerted effort across government to modernize retirement investment options. The completed OIRA review therefore represents a critical step in operationalizing the President’s vision, removing a major administrative obstacle for a proposal that could significantly widen the path for alternative assets in US defined-contribution retirement plans.

Crypto-linked Exposure Moves Closer to the $48 Trillion 401(k) Market

The current administration’s proactive stance on crypto in retirement plans marks a distinct departure from previous guidance. On May 28, 2025, the DOL took a decisive step by rescinding a 2022 compliance release that had previously urged fiduciaries to exercise "extreme caution" when contemplating cryptocurrency investments for 401(k) retirement plans. That earlier guidance reflected significant concerns about the nascent asset class’s volatility, speculative nature, and the nascent regulatory framework surrounding it. The rescission of this cautionary stance unequivocally signals a broader, more accommodative shift in the federal government’s approach toward allowing retirement-plan exposure to digital assets. This policy reversal is a testament to the growing mainstream acceptance and demand for digital assets, moving them from the periphery of investment options to the brink of institutional adoption within the retirement sector.

The U.S. retirement market represents an colossal pool of capital, reaching a record $48.1 trillion in financial assets as of September 30, 2025, according to a comprehensive report by the Investment Company Institute (ICI). This immense market encompasses various types of retirement plans, including defined-contribution plans like 401(k)s, defined-benefit plans, and individual retirement accounts (IRAs). Even a small allocation of this vast sum into digital assets could translate into billions, if not trillions, of dollars flowing into the cryptocurrency ecosystem, providing unprecedented institutional liquidity and legitimization. This potential influx of capital could not only bolster the valuations of leading cryptocurrencies like Bitcoin and Ethereum but also foster greater innovation and infrastructure development within the digital asset space.

Understanding the "Economically Significant" Impact and Fiduciary Duties

The "economically significant" label attached to the DOL proposal by OIRA underscores the profound implications this rule could have. Such a designation is reserved for rules that are likely to have an annual effect on the economy of $100 million or more, or adversely affect in a material way the economy, a sector of the economy, productivity, competition, jobs, the environment, public health or safety, or state, local, or tribal governments or communities. In this context, it signals that the federal government anticipates a substantial economic ripple effect from allowing alternative assets, including crypto, into 401(k) plans.

A central element of this debate revolves around fiduciary duty. Under the Employee Retirement Income Security Act of 1974 (ERISA), fiduciaries—those responsible for managing 401(k) plans—are legally obligated to act solely in the interest of plan participants and their beneficiaries. This includes exercising prudence, diversifying investments, and ensuring reasonable costs. The previous "extreme caution" guidance for crypto was rooted in concerns that its volatility and lack of a robust regulatory framework made it difficult for fiduciaries to meet these duties without undue risk.

The new proposal, by allowing or guiding the inclusion of digital assets, would likely come with new frameworks for fiduciaries to evaluate these assets responsibly. This could involve stringent due diligence requirements, specific guidance on custodial solutions, risk disclosure standards, and potentially limitations on allocation percentages. "This is not simply an open door for all crypto," commented a hypothetical retirement plan consultant. "The DOL will undoubtedly provide a roadmap for how fiduciaries can prudently offer these assets, likely emphasizing robust education for participants, highly secure custody, and a thorough understanding of the underlying technology and market dynamics."

The Rationale for Alternative Assets in Retirement Portfolios

The push to expand access to alternative assets beyond traditional stocks and bonds in retirement plans reflects a broader evolution in investment philosophy. Proponents argue that alternatives, such as private equity, real estate, and now digital assets, can offer several benefits:

- Diversification: They may have low correlation with traditional assets, potentially reducing overall portfolio risk during market downturns.

- Enhanced Returns: Some alternative assets have historically offered higher returns than traditional investments, though often accompanied by higher risk.

- Inflation Hedge: Assets like real estate and certain digital assets (e.g., Bitcoin with its fixed supply) are sometimes seen as potential hedges against inflation.

- Access to Growth Sectors: Digital assets represent an emerging technological and financial paradigm, offering exposure to innovation that might not be fully captured by public equities.

However, challenges remain. Alternative assets often come with higher fees, less liquidity, and complex valuation methodologies, requiring sophisticated due diligence from plan fiduciaries. The DOL’s forthcoming guidance will likely attempt to strike a balance between expanding access and safeguarding investor interests.

State-Level Momentum and Global Trends

The federal initiative is not occurring in a vacuum; several U.S. states have independently launched their own legal initiatives to facilitate the inclusion of digital assets as retirement plan assets, underscoring a nationwide demand. On February 25, 2026, Indiana lawmakers passed a significant bill that would mandate certain state retirement and savings plans to offer a self-directed brokerage option, which must include at least one cryptocurrency investment option, by July 1, 2027. This pioneering legislation would allow Indiana citizens to hold Bitcoin (BTC) and other digital assets as part of their retirement plans for the first time, setting a precedent for other states.

This domestic momentum is mirrored by international trends. As hinted by reports, major Australian pension funds, such as Hostplus, are actively considering crypto offerings amid growing demand from their members. This global exploration by institutional investors reflects a broader recognition of digital assets as a legitimate, albeit still evolving, asset class. "The move by the White House and DOL aligns with a global trend of increasing institutional acceptance of digital assets," noted a hypothetical crypto industry analyst. "Pension funds and sovereign wealth funds worldwide are looking for diversification and exposure to the digital economy. The U.S. is now signaling its intent to not be left behind in this critical financial evolution."

Looking Ahead: The Public Comment Period and Beyond

The upcoming 60-day public comment period will be critical. It will provide a platform for a wide array of voices, including consumer advocacy groups, financial advisors, crypto exchanges, traditional financial institutions, and individual investors, to weigh in on the proposed rule. Expect robust debate around issues such as:

- Investor Protection: How to ensure adequate safeguards for retirement savers, given crypto’s volatility and the potential for fraud.

- Fiduciary Liability: Clarifying the scope of fiduciary responsibility when offering digital assets.

- Custody and Security: Requirements for secure storage and management of digital assets within retirement plans.

- Education: The need for comprehensive educational resources for plan participants regarding the risks and benefits of crypto.

- Investment Vehicles: Specifying what types of crypto-linked investment vehicles (e.g., spot ETFs, futures ETFs, direct ownership through self-directed accounts) will be permissible.

Following the comment period, the DOL will review all submissions and may make revisions to the proposed rule before issuing a final rule. This entire process can take several months, but the completion of the OIRA review indicates that the federal government is committed to advancing this policy.

In conclusion, the White House’s greenlight on the DOL’s proposal for crypto in 401(k) plans marks an undeniable turning point for digital assets in the U.S. financial system. It signifies a maturation of the crypto market, a responsiveness from policymakers to evolving investment landscapes, and a potential new frontier for retirement savings. While the path to full implementation will involve further regulatory scrutiny and public discourse, this development unequivocally solidifies digital assets as a serious contender for a permanent place within the diversified portfolios of millions of American workers saving for their future.