This move by Representative Waters underscores the growing tension between financial innovation, particularly within the nascent cryptocurrency sector, and the established regulatory frameworks designed to ensure stability and protect consumers. The Federal Reserve’s decision earlier this month to grant Kraken Financial a limited-purpose master account was hailed by many in the crypto industry as a watershed moment. For years, numerous crypto-linked US companies have been actively pursuing direct access to the Federal Reserve’s payment systems, often facing significant hurdles and delays. This approval marked a crucial step towards integrating digital asset firms into the nation’s core financial infrastructure, potentially bypassing traditional intermediary banks that have historically been reluctant or unable to serve the crypto industry.

A master account provides direct access to Fedwire, the Federal Reserve’s real-time gross settlement system, which is the backbone of interbank payments in the United States. This direct access could fundamentally transform Kraken’s operations, enabling it to move money on the same secure and efficient rails used by commercial banks and credit unions. This means faster, cheaper, and more direct settlement of transactions, potentially reducing operational risks and costs associated with reliance on third-party banking partners. Without a master account, crypto firms must partner with traditional banks, which often means higher fees, slower settlement times, and the constant risk of de-banking due to regulatory uncertainties or risk aversion from the traditional financial sector.

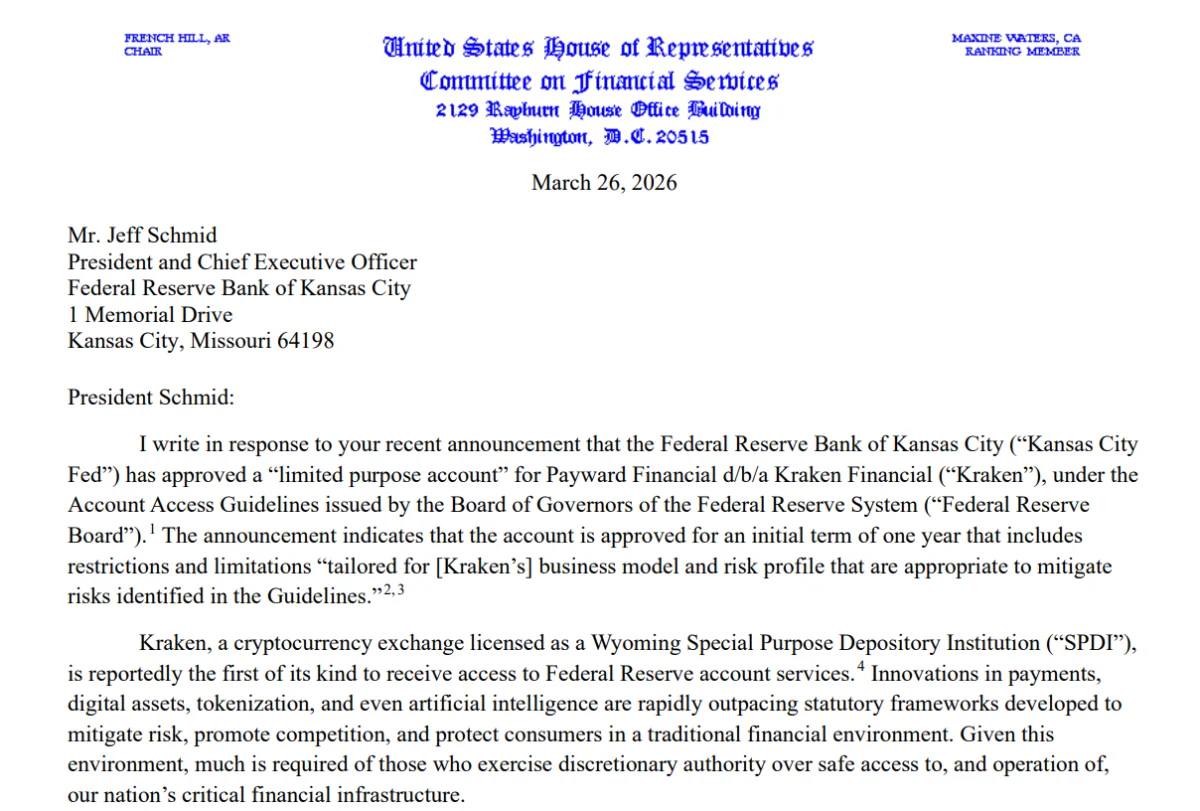

However, Representative Waters’ letter highlighted a critical lack of transparency surrounding the Kansas City Fed’s decision. She noted, "The Kansas City Fed’s announcement does not disclose specific information about Kraken’s access to the range of Federal Reserve financial services due to the confidentiality of business information provided by applicants." This confidentiality, while standard for some banking applications, raises concerns for Waters given the novel nature of a crypto firm gaining such access. Her demand for answers is rooted in the belief that "Answers to these questions are critical to ensuring that the process of approving Federal Reserve Bank account access is conducted consistently with the law, with impartiality, and in a manner that continues to foster a safe and efficient payment system." This statement reflects a broader sentiment among some lawmakers and regulators that the rapid pace of technological change in finance necessitates enhanced scrutiny, not reduced transparency.

Beyond procedural transparency, Waters explicitly argued that Kraken’s access to the Federal Reserve’s payment system inherently raises significant policy, regulatory, and consumer protection concerns. She emphasized that full transparency and a clear legal grounding are absolutely essential to ensure that any potential risks associated with this integration are properly identified, understood, and mitigated. Her letter articulated a fundamental challenge facing regulators today: "Innovations in payments, digital assets, tokenization, and even artificial intelligence are rapidly outpacing statutory frameworks developed to mitigate risk, promote competition, and protect consumers in a traditional financial environment." This observation underscores the dilemma for policymakers who must balance fostering innovation with upholding their core mandate of financial stability and consumer welfare. In such an environment, Waters concluded, "much is required of those who exercise discretionary authority over safe access to, and operation of, our nation’s critical financial infrastructure."

The context of this approval is further illuminated by the experiences of other crypto-linked entities. For instance, Caitlin Long’s Custodia Bank, a Wyoming-chartered special purpose depository institution (SPDI), has been locked in a protracted legal battle with the Federal Reserve over its master account application. Custodia filed a court petition in late 2022 to renew its bid after facing significant delays and an eventual rejection from the Federal Reserve Board of Governors. Similarly, crypto platform Anchorage Digital Bank, another federally chartered institution, applied for an account last year, and Ripple has sought access through its acquisition of Standard Custody & Trust Company. The fact that Kraken Financial, also a Wyoming SPDI, successfully secured a master account while others faced prolonged struggles or outright rejections, highlights either a shift in the Fed’s stance or unique circumstances surrounding Kraken’s application that Waters and others wish to understand. This disparity fuels the call for transparency and a clear, consistent framework for evaluating such applications.

Representative Waters’ stance on this issue is consistent with her long-standing and well-documented skepticism towards the cryptocurrency industry. Crypto advocacy group Stand With Crypto, which maintains a scorecard for US politicians based on their public statements and voting behavior regarding digital assets, lists Waters as "strongly against crypto." This designation is based on five recorded statements and six votes against crypto-related legislation, including key bills like the Digital Asset Market Clarity Act and the GENIUS Act. Her concerns are not new; she has previously called for heightened oversight of the Securities and Exchange Commission (SEC) concerning its approach to crypto enforcement, demanding a hearing with then-SEC Chair Paul Atkins last year, citing worries about the agency’s dismissal of certain crypto enforcement cases. Her consistent legislative and public record demonstrates a deep-seated caution regarding the risks she perceives in the unregulated or under-regulated aspects of the digital asset space, including potential for illicit finance, market manipulation, and consumer exploitation.

The debate surrounding master account access for non-bank financial institutions, particularly those in the crypto sector, has been a contentious one within the Federal Reserve itself. The Fed’s August 2022 guidelines for evaluating master account applications aimed to create a more transparent and consistent process, categorizing institutions into three tiers based on their regulatory supervision. Wyoming SPDIs, like Kraken Financial and Custodia, fall into a category that requires a higher level of scrutiny due to their novel charters and varying degrees of state-level oversight. The Kansas City Fed’s decision, therefore, suggests that Kraken Financial was able to satisfy the rigorous criteria outlined in these guidelines, at least to the satisfaction of that particular Reserve Bank. However, the broader Federal Reserve System, including the Board of Governors, has often taken a more cautious approach, reflecting internal divisions and a desire to move slowly when integrating new, potentially disruptive financial technologies.

The implications of Waters’ inquiry are far-reaching. Should the Kansas City Fed’s response be deemed insufficient or unsatisfactory, it could lead to further congressional hearings, potential legislative action to clarify or restrict master account access for certain types of institutions, or increased pressure on the Federal Reserve to issue more detailed public guidance. The outcome will also serve as a crucial test case for the future integration of crypto firms into the traditional financial system. If Kraken’s access proves successful and well-managed from a risk perspective, it could pave the way for other eligible crypto institutions. Conversely, if significant unforeseen risks emerge or if Waters’ concerns are validated, it could lead to a retrenchment in regulatory openness towards crypto.

Ultimately, the confrontation between Representative Waters and the Federal Reserve Bank of Kansas City highlights a pivotal moment in the evolution of financial regulation in the digital age. It pits the promise of innovation and increased efficiency, championed by the crypto industry, against the imperative of robust regulatory oversight and consumer protection, advocated by veteran lawmakers like Waters. Her demand for answers is not merely an administrative query; it is a significant political and regulatory statement, emphasizing that access to the nation’s critical financial infrastructure cannot be granted without full transparency and an unwavering commitment to mitigating the inherent risks posed by novel financial technologies. The resolution of this inquiry will undoubtedly shape the trajectory of cryptocurrency integration into the mainstream financial system for years to come.