Fidelity Investments, a global asset management giant with trillions under management, has emphatically urged the U.S. Securities and Exchange Commission (SEC) to accelerate the development of a robust and comprehensive regulatory framework for broker-dealers seeking to engage with crypto assets. In a detailed submission delivered on Friday, the financial powerhouse stressed the critical need for clear guidelines on how traditional financial institutions can responsibly offer, custody, and trade tokenized securities and other digital assets within alternative trading systems (ATS). This significant intervention came as a direct response to a call for comments issued earlier this month by the SEC’s dedicated Crypto Task Force, signaling an escalating dialogue between Wall Street and Washington over the future of digital finance.

The asset manager’s letter, penned by its general counsel, Roberto Braceras, underscored the urgent imperative for the SEC to establish "clear rules of the road" for tokenized securities trading. This includes not only assets issued by broker-dealers themselves but, crucially, also those issued by third parties, which represent a vast and growing segment of the digital asset landscape. Fidelity’s position highlights the inherent complexities and unique characteristics of tokenized instruments, which often diverge significantly from traditional securities in their issuance structures, underlying legal frameworks, and valuation methodologies. Without a definitive regulatory blueprint, financial institutions face substantial uncertainty, hindering innovation and broader institutional adoption of these transformative technologies.

A core challenge identified by Fidelity lies in the multifaceted nature of tokenized instruments themselves. For instance, tokenized real-world assets (RWAs) represent a diverse spectrum of asset classes, ranging from traditional equities and corporate bonds to illiquid assets like real estate, private credit, and even intellectual property or fine art. Each of these underlying assets brings its own set of legal, operational, and valuation considerations, which become further complicated when translated onto a blockchain. The letter meticulously explained that "Tokenization models vary significantly in structure and in the rights afforded to holders," presenting a regulatory labyrinth for existing frameworks.

Fidelity elaborated on the critical distinction between different tokenization models. In some scenarios, a crypto asset may merely represent a holder’s indirect interest in an underlying security, akin to a beneficial ownership through a securities entitlement. In others, the crypto asset itself could constitute a securities-based swap, a more complex derivative instrument that, under current regulations, is typically restricted to "eligible contract participants" – sophisticated institutional investors. The regulatory treatment of these two distinct models varies dramatically, impacting everything from investor protection requirements to capital allocation and reporting obligations. The absence of clear guidance on how to classify and regulate these nuanced structures creates a significant impediment for broker-dealers looking to innovate within the tokenized asset space.

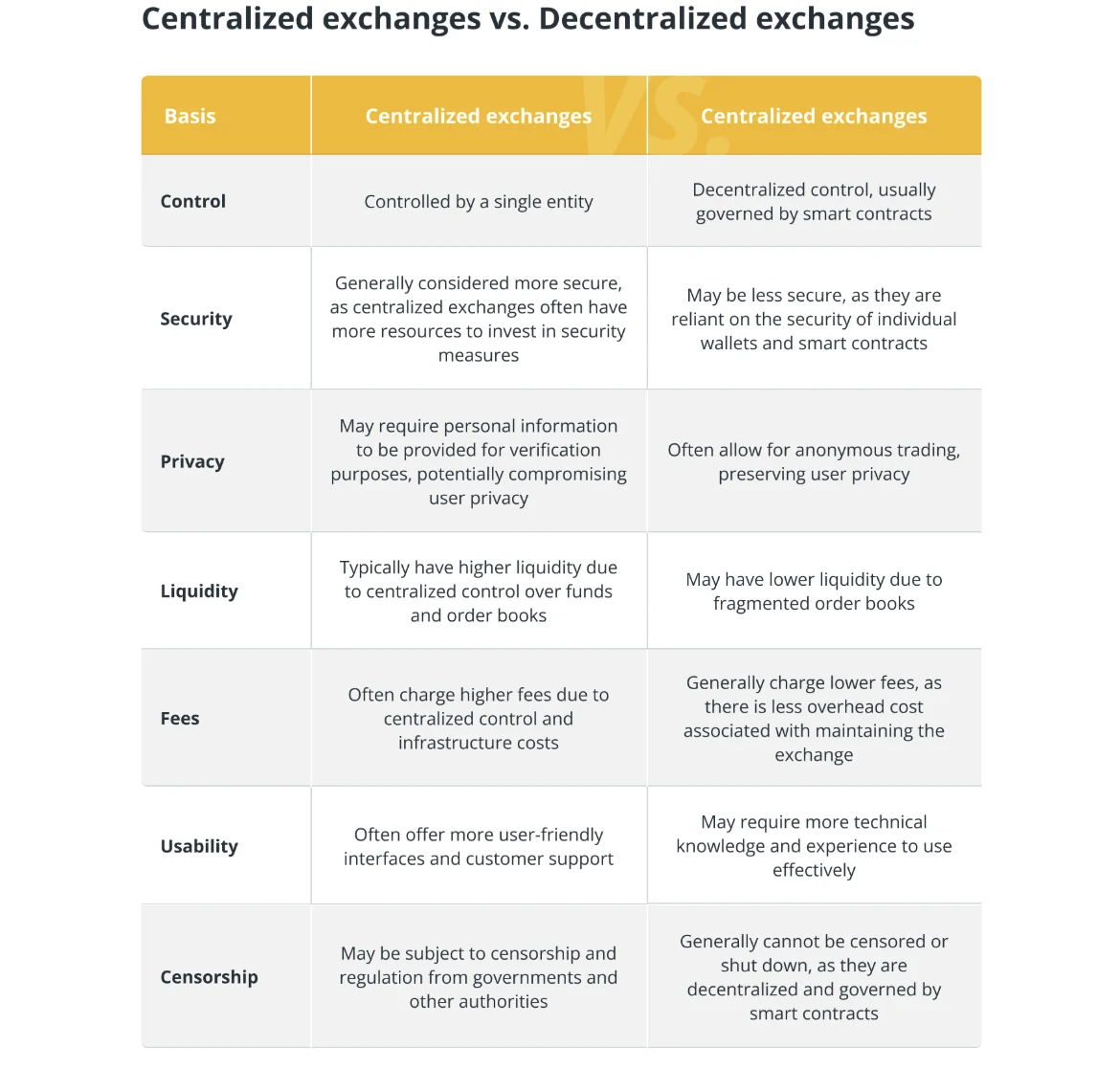

Beyond the specificities of tokenized securities, Fidelity also urged the SEC to proactively address and bridge the burgeoning regulatory gap between centralized (CeFi) and decentralized (DeFi) trading systems. The traditional financial ecosystem, characterized by intermediaries like brokers and exchanges, operates under well-established rules designed for centralized authority and oversight. DeFi, by contrast, relies on distributed ledger technology (DLT) and smart contracts to facilitate peer-to-peer transactions without the need for traditional intermediaries. Fidelity’s call to "consider how intermediated and disintermediated trading venues can evolve and coexist" reflects a forward-looking perspective, acknowledging that both models are likely to play significant roles in the future of finance. The regulatory challenge lies in fostering innovation in DeFi while ensuring adequate investor protection, market integrity, and financial stability, without stifling the inherent benefits of decentralization.

A significant hurdle for DeFi’s integration into a regulated framework, as highlighted by Fidelity, is the overhaul of existing reporting rules. Traditional financial reporting mechanisms are predicated on the existence of a central authority capable of generating detailed financial statements, transaction logs, and audit trails. Decentralized trading platforms, by their very design, lack such a central authority. This architectural difference means that requiring DeFi platforms to adhere to conventional reporting standards would impose an "undue burden" and, in many cases, be technically unfeasible. Fidelity’s recommendation suggests that the SEC must explore innovative reporting solutions that leverage the inherent transparency and immutability of distributed ledger technology, potentially focusing on on-chain data analytics and smart contract auditing, to achieve regulatory oversight without compromising the decentralized ethos.

Furthermore, Fidelity advocated for the SEC to issue explicit guidance permitting broker-dealers to leverage distributed ledger technology (DLT) not only for ATS but also for other critical recordkeeping purposes. DLT offers the potential for enhanced efficiency, greater transparency, immutable record-keeping, and near real-time settlement, which could revolutionize back-office operations and significantly reduce operational risks and costs. However, without clear regulatory approval and guidance, firms are hesitant to fully embrace DLT for fear of non-compliance with existing, often anachronistic, record-keeping requirements. Enabling broker-dealers to utilize DLT for these functions would streamline processes, reduce "undue burden," and align regulatory expectations with technological advancements.

The Securities and Exchange Commission, under the leadership of Chairman Paul Atkins – a figure who has consistently voiced support for modernizing financial markets – has indeed shown increasing openness to the concept of 24/7 capital markets and the potential of tokenized trading. Atkins, a former SEC Commissioner and a vocal advocate for innovation in financial services, has often emphasized the need for regulatory frameworks to adapt to new technologies rather than impede them. This forward-leaning perspective has translated into tangible actions, such as the SEC’s regulatory approval for financial companies like Nasdaq to experiment with tokenized trading pilots. These pilot programs are crucial testing grounds, allowing regulators and market participants to explore the practical implications and potential benefits of DLT-based financial infrastructure in a controlled environment. The overarching goal is to foster an environment where innovation can thrive while robust investor protection and market integrity are maintained.

This evolving regulatory landscape is also shaped by a broader consensus among U.S. financial regulators regarding the treatment of tokenized securities. A joint policy statement published in March by the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) unequivocally stated that tokenized securities are subject to the same banking capital requirements as the underlying assets they represent. This principle, often summarized as "same activity, same risk, same regulation," signifies a unified stance that the technological wrapper of an asset does not alter its fundamental nature or the risks it poses to the financial system. The agencies clarified, "The technologies used to issue and transact in a security do not generally impact its capital treatment," providing a foundational understanding for how banks should account for and capitalize their holdings of tokenized equities, debt instruments, real estate investment trusts (REITs), and other securitized assets. This consistent approach aims to prevent regulatory arbitrage and ensure that the adoption of DLT does not introduce new systemic risks into the banking sector.

Fidelity’s comprehensive letter underscores a pivotal moment in the intersection of traditional finance and the burgeoning digital asset ecosystem. The firm’s proactive engagement with the SEC reflects a growing recognition within established financial institutions that tokenization and decentralized finance are not fleeting trends but foundational shifts that will reshape global capital markets. While the promise of enhanced efficiency, greater liquidity, fractional ownership, and 24/7 trading capabilities offered by digital assets is immense, so too are the regulatory challenges. Issues of investor protection, market manipulation, financial stability, and anti-money laundering (AML) compliance must be meticulously addressed. Fidelity’s request for clarity is a plea not just for itself, but for the entire industry, seeking a coherent and predictable regulatory environment that can unlock the full potential of these transformative technologies while safeguarding market participants and maintaining the integrity of the financial system. The ongoing dialogue between industry leaders and regulators will undoubtedly shape the future trajectory of digital finance in the United States and beyond.