Across the globe, a paradoxical situation persists where, despite the burgeoning institutional adoption of digital assets and their increasing integration into mainstream finance, individual crypto users frequently face the archaic reality of frozen bank accounts and blocked transfers. This persistent friction between the traditional banking system and the burgeoning crypto economy highlights a fundamental disconnect, creating significant hurdles for everyday users and legitimate businesses operating in the digital asset space.

Panos Mekras, co-founder and CEO of blockchain fintech Anodos Labs, vividly recalls the nascent days of his crypto journey in Greece during the late 2010s. Back then, the landscape was markedly hostile; most Greek banks actively prevented transfers to crypto exchanges. Mekras’s experience was emblematic: a series of blocked card payments, until one bank finally allowed his transactions, but not without a stern interrogation. He was made to acknowledge the "risky" nature of the counterparty, a paternalistic warning that underscored the banks’ deep-seated apprehension. Mekras recounted to Cointelegraph that these early rejections were not isolated incidents but rather symptomatic of a systemic issue where traditional financial institutions inherently label digital assets as high-risk. This blanket categorization often led to arbitrary account closures or sudden freezes, frequently without any prior warning or clear explanation, ultimately compelling his business to pivot towards relying almost exclusively on onchain tools and payment rails to circumvent these banking impediments.

Despite the passage of time and the dramatic evolution of public perception surrounding crypto – from a niche speculative asset class to a recognized infrastructure layer poised to underpin future financial products – Mekras confirms that these banking barriers remain strikingly prevalent. As recently as "a few months ago," he encountered the very same issues. "I tried to send money from an exchange to Revolut, and they froze my account for three weeks. I had no access to my [funds] during that time," he lamented, underscoring the severe operational and personal disruption that such actions inflict on individuals and businesses alike, even those engaging with seemingly reputable and regulated platforms.

The Enduring Shadow of Crypto Debanking

Mekras’s experience is far from unique; countless crypto holders globally echo similar complaints, presenting a stark contrast to the narratives of banks announcing ambitious expansions into crypto custody and blockchain initiatives. This dichotomy suggests a significant gap between institutional strategy and retail service delivery. A comprehensive report published in January by the UK Cryptoasset Business Council, titled "Locked Out: Debanking the UK Digital Asset Economy," laid bare the widespread nature of this problem. The report found that bank transfers to exchanges were routinely blocked or subjected to extensive delays, with approximately 40% of all payments encountering some form of restriction. Alarmingly, 80% of crypto exchanges operating in the UK reported a noticeable increase in banking friction over the preceding year. The council issued a stark warning that blanket bans and arbitrary transaction limits were frequently imposed without any discernible regard for the legal standing or regulatory compliance of the crypto exchanges involved, effectively penalizing legitimate enterprises and users.

Revolut, notably, was identified in the UK council’s study as one of only two banks that permit both bank transfers and debit card usage for crypto transactions. Yet, it is precisely this platform where Mekras alleges his recent account freeze occurred. Revolut operates under a unique regulatory structure, functioning as an authorized UK bank "with restrictions," signifying that it is still in the process of scaling up its full banking operations. Additionally, it holds a full European Union banking license through Lithuania and offers integrated crypto trading services directly within its app. When questioned about these incidents, a Revolut spokesperson clarified to Cointelegraph that account freezes are considered a "last-resort" customer protection measure, meticulously implemented to ensure compliance with stringent Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. The spokesperson elaborated, stating, "A temporary freeze may occur if our systems detect irregular activity. This could be a combination of a few factors, such as if a customer interacts with a platform frequently exploited by fraudsters, or we believe that the funds in question may be the proceeds of crime or sanctions circumvention." While acknowledging the necessity of such measures, the representative added that since October 1st, a remarkably low 0.7% of Revolut accounts where customers deposited crypto funds were ultimately restricted or frozen following thorough investigation. This figure, while statistically small, does little to assuage the frustration of those individuals who find themselves among that fraction, facing prolonged fund inaccessibility.

When Traditional Banks Close Doors, Users Seek Onchain Alternatives

In some regions, the restrictions on crypto are far more extreme, pushing users towards entirely unregulated and often perilous alternatives. In jurisdictions like China, where official crypto on- and off-ramps are legally impossible, users are forced to resort to peer-to-peer (P2P) platforms or even illicit black markets to trade digital assets, exposing them to heightened risks of fraud and exploitation. While China represents the most stringent end of this regulatory spectrum, other nations have demonstrated a more pragmatic evolution in their approach. Nigeria, for instance, initially imposed a ban on crypto transactions and even blocked P2P platforms. However, recognizing the burgeoning adoption and economic potential, the country formally recognized digital assets as securities in 2025, signaling a significant policy shift aimed at integrating crypto into its regulated financial framework.

Similar patterns of banking friction have also been observed in the United States, prompting lawmakers and industry stakeholders to coin the term "Operation Chokepoint 2.0." This term describes the alleged informal guidance from federal regulators that subtly, yet effectively, discouraged banks from establishing or maintaining relationships with crypto companies. The original "Operation Choke Point" was a controversial initiative where enforcement agencies were accused of pressuring banks to sever ties with politically contentious industries, such as payday lenders and firearms sellers, demonstrating a historical precedent for regulatory overreach.

A significant turning point occurred in January 2025 when Donald Trump assumed the US presidency, swiftly initiating a push for crypto-friendly policies, aiming to position the world’s largest economy as the "crypto capital" of the world. This political shift seemingly paved the way for official recognition of crypto debanking issues. In December of the same year, the US Office of the Comptroller of the Currency (OCC) released its findings from a comprehensive review of debanking practices by nine of the country’s largest banks, explicitly including crypto among the affected sectors. Concurrently, the OCC published an interpretive letter unequivocally confirming that banks are indeed permitted to facilitate crypto transactions in a broker-like capacity, providing much-needed regulatory clarity.

Despite this positive momentum and clearer regulatory directives, individual users continue to report that the traditional banking sector remains largely unwilling to service accounts exposed to cryptocurrencies. Mekras asserts, "This is still the case [and] there are still anti-crypto positions. Some have even said publicly that they are not willing to support crypto activity or engage with the industry." This resistance from some banks, even in the face of evolving regulations, can be attributed to various factors, including perceived reputational risks, the high costs associated with implementing specialized compliance frameworks for digital assets, and a lingering lack of internal expertise. Mekras argues that users might consider a complete detachment from the traditional banking system, opting to manage all finances exclusively onchain. While theoretically appealing, this solution remains largely impractical for most businesses and individuals who still require reliable access to fiat on- and off-ramps for essential functions like paying salaries, taxes, suppliers, and managing daily expenses. The reality is that a truly functional financial ecosystem necessitates seamless interoperability between traditional and decentralized finance.

Traditional Banking’s Inevitable Turn Toward Blockchain Infrastructure

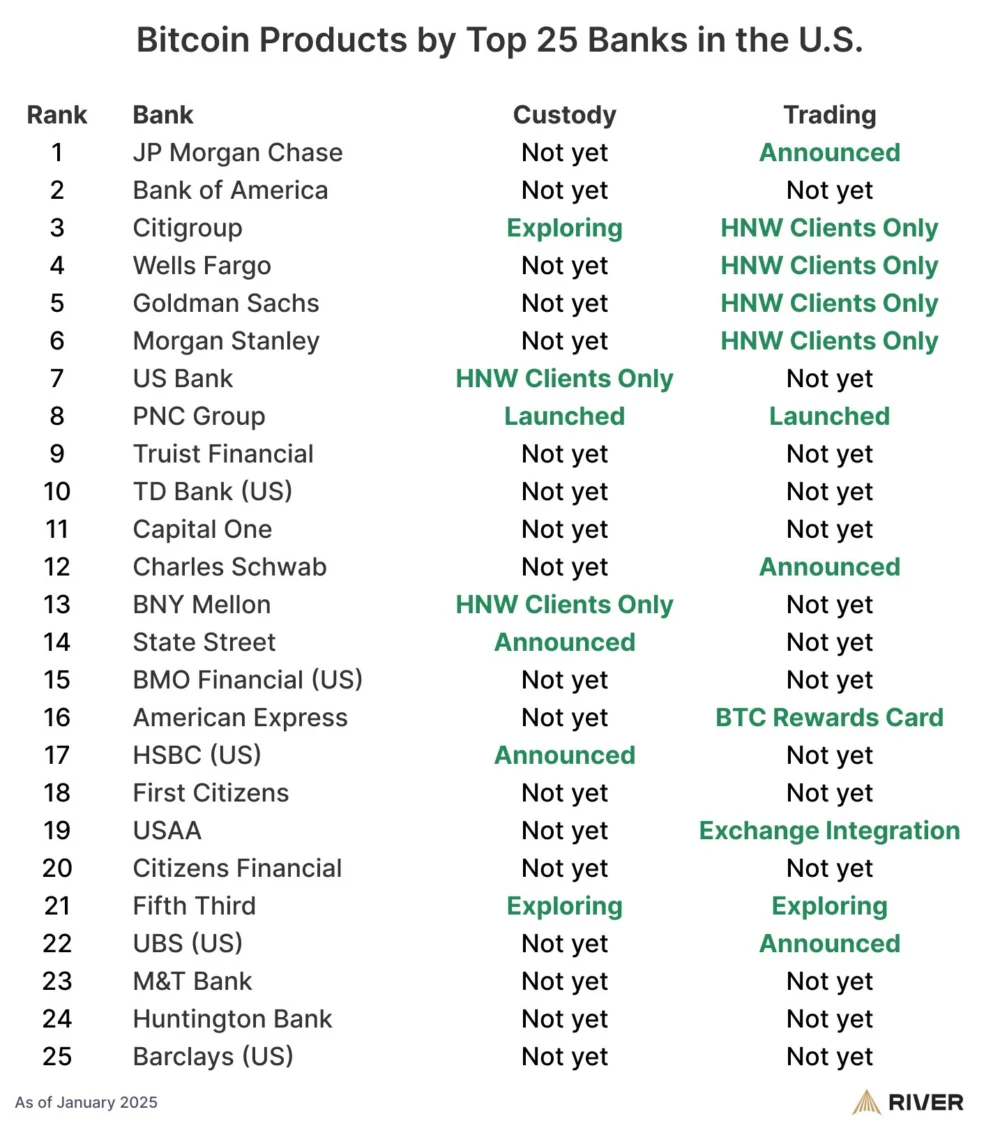

Paradoxically, even as retail users grapple with these pervasive banking frictions, there has been a notable and undeniable global shift in how traditional financial institutions engage with the underlying technology of crypto. In recent years, major banks and established financial infrastructures are increasingly investing in and building products and services inextricably tied to Web3. In the United States, a staggering 60% of the top 25 banks are reportedly either already offering or actively planning to offer Bitcoin-related services, encompassing everything from institutional-grade custody solutions to trading and advisory services. This indicates a growing acknowledgment of digital assets as a legitimate, if still challenging, asset class for sophisticated investors.

Across Europe, the implementation of the Markets in Crypto-Assets Regulations (MiCA) has been a watershed moment, providing a clear and comprehensive regulatory framework that has emboldened legacy exchanges and financial groups to introduce regulated services such as crypto custody and settlement. This regulatory certainty is critical for fostering institutional confidence. In the United Kingdom, for instance, HSBC’s advanced blockchain platform was strategically selected to support pilot issuances of tokenized government bonds, a groundbreaking initiative that signals the mainstreaming of distributed ledger technology within sovereign financial instruments.

Against this backdrop of accelerating institutional adoption, companies actively working to bridge the chasm between traditional banks and blockchain technology contend that the persistent challenges leading to account freezes are primarily linked to fundamental tooling gaps and outdated risk frameworks within banking institutions. Eyal Daskal, CEO of Crymbo – a blockchain infrastructure platform designed for institutions – explained to Cointelegraph, "The problem is that there’s a huge amount of friction because traditional banks don’t really have the internal infrastructure to interpret blockchain data in a way that fits inside their existing risk and compliance frameworks." He elaborated on the core issue, describing a situation where banks often default to overly cautious measures precisely because they lack the sophisticated tools and expertise required to effectively link onchain activity with the established identity and compliance signals they traditionally rely upon. "If crypto is involved, they block the account and treat it as out of scope. It’s the simplest option for them because they don’t have the tools to assess it properly," Daskal concluded. This default to restriction, rather than informed assessment, underscores the urgent need for specialized fintech solutions and greater investment in blockchain literacy within the traditional banking sector.

Ultimately, while cryptocurrency is undeniably cementing its place within the financial mainstream, for a vast segment of individual users and smaller businesses, access to basic banking services remains precariously dependent on the archaic capabilities of a bank’s risk engine to comprehend and appropriately assess onchain transactions. Until this critical technological and knowledge gap is decisively closed, the striking dichotomy between the financial industry’s enthusiastic institutional embrace of blockchain and the ongoing, frustrating retail friction faced by everyday crypto users is set to persist, creating an uneven and often prohibitive landscape for participants in the digital economy.