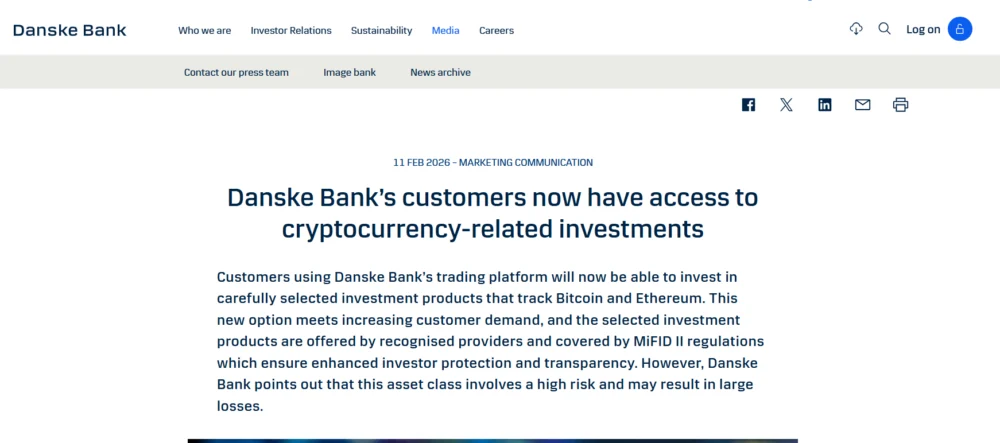

Danske Bank, a towering financial institution holding the undisputed position as the largest bank in Denmark and a significant retail banking force across Northern Europe, serving a vast clientele exceeding five million customers, has announced a landmark decision to allow its clients to purchase Bitcoin and Ether exchange-traded products (ETPs). This pivotal shift in policy sees the bank integrating these digital asset investment vehicles from prominent asset managers BlackRock and WisdomTree directly into its established eBanking and Mobile Banking platforms, marking a new era of access for its customers.

The new offering, formally unveiled in a press release on Wednesday, represents a calculated move by Danske Bank to cater to an evolving financial landscape and burgeoning investor interest in digital assets. Crucially, the service is exclusively available to self-directed investors – those clients who actively manage their portfolios and execute trades through the bank’s platforms without seeking or receiving direct investment advice. This deliberate framing underscores the bank’s cautious yet responsive approach, explicitly attributing the decision to "increasing customer demand" and the advent of "improved regulation," particularly referencing the European Union’s groundbreaking Markets in Crypto Assets (MiCA) regime. MiCA, a comprehensive regulatory framework, aims to bring clarity and stability to the crypto market within the EU, providing a much-needed layer of legal certainty that has historically been absent.

Initially, Danske Bank is making available three "carefully selected" ETPs. This curated selection includes two products tracking the performance of Bitcoin (BTC) and one focused on Ethereum (ETH), all underwritten by industry giants BlackRock and WisdomTree. The involvement of such traditional financial heavyweights in the crypto ETP space not only lends considerable credibility to these products but also signals a broader institutional acceptance of digital assets. These ETPs are furthermore covered by the Markets in Financial Instruments Directive II (MiFID II) rules, a robust EU legislative framework designed to ensure high standards of investor protection and cost transparency. Danske Bank emphasizes that investing via these regulated ETPs offers distinct advantages over the direct ownership of cryptocurrencies, citing enhanced ease of trading, familiar regulatory oversight, and critically, the secure custody solutions provided by established financial entities. This approach mitigates some of the operational and security concerns often associated with individual crypto holdings.

Kerstin Lysholm, the head of investment products and offerings at Danske Bank, elaborated on the bank’s strategic rationale in the official release. She noted that cryptocurrencies have steadily matured and gained recognition as a legitimate asset class within the broader financial ecosystem. This evolving perception has, in turn, led to an "increasing number of enquiries from customers wanting the option of investing in cryptocurrencies as part of their investment portfolio." Lysholm further articulated that the maturation of regulatory frameworks, particularly MiCA, has "generally increased confidence in cryptocurrencies" among both institutional players and retail investors. This newfound regulatory clarity and investor confidence have collectively led the bank to conclude that "the time is ripe" to introduce such products, albeit with a clear acknowledgment that clients must accept the "very high risks" inherently involved in cryptocurrency investments.

This significant policy shift by Danske Bank is particularly noteworthy given its historical stance of extreme caution, and at times, outright prohibition, regarding digital assets. As recently as 2018, the bank publicly declared its negative outlook on cryptocurrencies. It implemented a strict policy that barred any trading of cryptocurrencies or related instruments on its proprietary platforms. At the time, Danske Bank issued stern warnings to its customers against investing in digital assets, citing profound concerns related to transparency, the nascent and often ambiguous regulatory environment, extreme price volatility, and the pervasive risks of financial crime and money laundering associated with the then-unregulated crypto market. The period around 2018 was marked by significant market speculation, price bubbles, and a lack of clear legal frameworks globally, making traditional financial institutions highly apprehensive.

By 2021, Danske Bank had subtly updated its stance, issuing a four-point notice that, while still emphasizing that it "wouldn’t offer any cryptocurrency services" itself, it would no longer "interfere with transactions coming from crypto platforms." This represented a nuanced, albeit cautious, step towards acknowledging the growing prevalence of digital assets and allowing customers a degree of autonomy in managing their crypto investments outside the bank’s direct purview. This gradual evolution underscores the pressure traditional banks face from both market forces and their customer base to adapt to new financial technologies.

Despite the introduction of ETPs, Lysholm emphasized that Danske Bank continues to view crypto as "opportunistic investments" rather than a fundamental component of a long-term, diversified investment portfolio. She made it unequivocally clear that providing access to these ETPs "should not be seen as a recommendation of the asset class" by the bank. This cautious communication strategy aims to manage client expectations and reinforce the inherent risks. To further mitigate these risks and ensure responsible investing, the bank is integrating a rigorous suitability check into the investment flow. Before any trading can commence, customers are required to answer a series of questions designed to ascertain their experience and knowledge, ensuring they possess a comprehensive understanding of the unique risks and characteristics associated with crypto ETPs. This due diligence process aligns with MiFID II requirements and reinforces the bank’s commitment to investor protection, even in a high-risk asset class. The inherent volatility of cryptocurrencies means that investments can result in substantial and rapid losses, a reality the bank is keen for its clients to fully comprehend.

Danske Bank’s move is not an isolated incident but rather indicative of a broader and accelerating trend among European lenders to embrace, albeit cautiously, regulated crypto offerings. The continent, particularly with the advent of MiCA, is positioning itself as a leader in creating a clear regulatory environment for digital assets, which in turn encourages institutional participation.

One notable example is BBVA, Spain’s second-largest bank, which, in 2025, expanded its Bitcoin and Ether trading and custody services to all retail customers in Spain. This expansion followed a successful pilot program that initially targeted private banking clients in Switzerland, showcasing a phased and strategic entry into the crypto market. BBVA’s journey highlights a common pattern: testing the waters with a smaller, often more sophisticated client base, before broadening access. The move by such a major Spanish bank underscores the increasing mainstream acceptance of crypto as an investable asset class within established financial systems.

Similarly, Germany’s Deutsche Bank, another European banking behemoth, is reportedly preparing to roll out its own crypto custody service in 2026. This initiative is being developed in collaboration with Bitpanda, a leading European crypto platform, and Taurus, a Swiss digital asset firm specializing in enterprise-grade infrastructure for digital assets. Deutsche Bank’s entry into crypto custody would signify a profound shift, offering institutional-grade security and compliance for digital asset holdings, which is crucial for attracting larger institutional investors and corporate clients. These developments illustrate a continental shift where major financial institutions are no longer shying away from digital assets but are actively seeking compliant and secure ways to integrate them into their offerings. The regulatory clarity provided by frameworks like MiCA is a key enabler for these strategic pivots, offering a predictable legal environment that minimizes compliance risks.

The collective actions of Danske Bank, BBVA, and Deutsche Bank paint a clear picture of an evolving financial landscape in Europe. As regulatory frameworks continue to mature and customer demand for diversified investment opportunities grows, more traditional financial institutions are expected to follow suit. This institutional embrace of ETPs for Bitcoin and Ethereum signifies a crucial step in bridging the gap between traditional finance and the nascent digital asset economy, potentially leading to increased liquidity, stability, and mainstream adoption of cryptocurrencies across the European Union and beyond. The cautious but deliberate approach taken by these banks, emphasizing investor protection and regulatory compliance, sets a precedent for how traditional finance can responsibly integrate the innovative potential of digital assets.

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently. Read our Editorial Policy https://cointelegraph.com/editorial-policy