For months leading up to the unexpected escalation in the Middle East, Bitcoin had languished in a frustrating sideways trading pattern, struggling to find clear directional momentum, while traditional safe haven assets, most notably gold, ascended to unprecedented record highs. During this period, the prevailing market sentiment firmly positioned gold as the undisputed asset of choice for investors seeking refuge from economic uncertainties. Persistent inflation concerns, fueled by global supply chain disruptions and expansionary monetary policies, coupled with a steady build-up of geopolitical tensions across various flashpoints, underscored gold’s historical appeal as a tangible store of value. Bitcoin, despite its proponents’ fervent claims of being "digital gold" and a hedge against fiat currency debasement, largely failed to live up to this safe haven expectation, instead mirroring the broader risk-on/risk-off sentiment of equity markets.

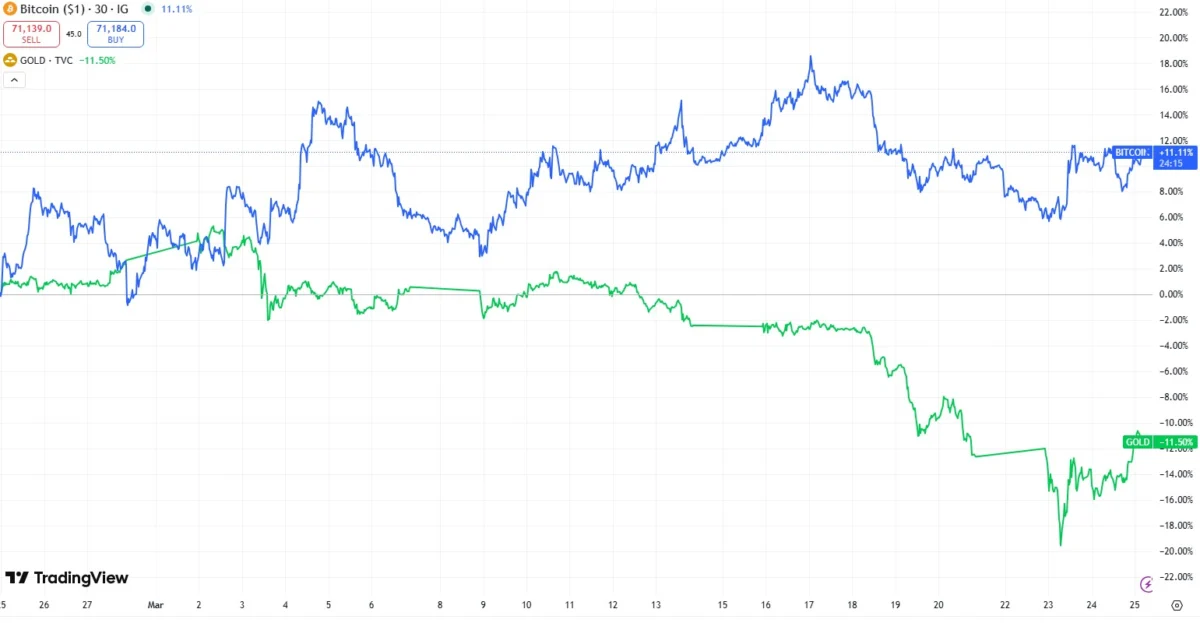

However, the narrative began to shift dramatically following the initial strikes launched by the U.S. and Israel on Iran on February 28. In the immediate aftermath of the news, Bitcoin experienced a sharp, albeit short-lived, sell-off, plummeting to $63,176. This knee-jerk reaction initially reinforced the view that it behaved like any other risk asset susceptible to geopolitical shocks. Yet, in the subsequent weeks, a remarkable turnaround unfolded. As of the latest Wednesday figures, Bitcoin had staged an impressive recovery, surging approximately 12% to reach $71,012, challenging the established perception and prompting a re-evaluation of its role in times of crisis.

In stark contrast to Bitcoin’s rally, gold, the supposed ultimate safe haven, witnessed a significant downturn. Rising global oil prices, directly impacted by the escalating conflict and concerns over supply disruptions, reignited fears of persistent inflation. This renewed inflationary pressure weighed heavily on gold, which recorded an 11% decline last week, marking its most substantial weekly loss since 1983. This dramatic divergence, visually captured in market data, suggested that Bitcoin had surprisingly outperformed gold since the conflict began, prompting a crucial question: was Bitcoin finally proving its mettle as a safe haven, or were other factors at play?

Despite its recent price resilience, many market analysts remain cautious, suggesting that Bitcoin’s behavior still aligns more closely with that of a risk asset rather than a true safe haven. Jonatan Randin, a senior market analyst at PrimeXBT, articulated this sentiment succinctly, stating, “It sells off alongside equities during geopolitical shocks. It’s range-bound and showing weakness within a broader downtrend. That’s not safe haven behavior.” Randin’s perspective underscores the expectation that a genuine safe haven asset should either remain stable or appreciate during periods of heightened uncertainty, ideally exhibiting an inverse or uncorrelated relationship with traditional risk assets like stocks. Bitcoin’s initial dip and subsequent recovery, while impressive, occurred within a broader context of volatility that still saw it reacting to major market events in a manner consistent with riskier investments.

Liquidity: The "Dominant" Driver of Bitcoin’s Price

In recent years, Bitcoin’s price movements have been observed to react to a wide array of global news events, ranging from significant geopolitical shocks to even social media posts by influential figures, such as former U.S. President Donald Trump. While these headline-driven fluctuations can be dramatic, they often prove to be transient. Matthew Pinnock, co-founder of the decentralized finance project Altura, provided a deeper insight into Bitcoin’s fundamental drivers, telling Cointelegraph that global liquidity remains the paramount force dictating Bitcoin’s price trajectory. According to Pinnock, macro conditions consistently outweigh the short-term volatility induced by breaking news.

Pinnock explained that "BTC is trading as a high-beta liquidity asset." To unpack this, "high-beta" implies that Bitcoin’s price tends to move with greater volatility than the overall market, amplifying both upward and downward swings. As a "liquidity asset," its value is particularly sensitive to the overall availability of capital in the global financial system. Consequently, tighter financial conditions—characterized by higher real yields, a strengthening U.S. dollar, and subdued inflows into exchange-traded funds (ETFs)—directly reduce the amount of marginal capital available in the market. This reduction in available capital, in turn, exerts significant downward pressure on Bitcoin’s price, irrespective of geopolitical events.

This perspective is robustly supported by extensive research. A September 2024 analysis, meticulously compiled by Sam Callahan of the treasury company OranjeBTC, revealed a striking correlation: Bitcoin’s price exhibited a remarkable 0.94 correlation with global liquidity between May 2013 and July 2024. A correlation coefficient of 0.94 is exceptionally high, indicating that Bitcoin’s price movements are almost entirely in sync with changes in global liquidity. For context, a perfect positive correlation is 1.0.

Callahan’s analysis further illustrated this point by showing that Bitcoin moved in the same direction as global M2 (a broad measure of money supply including cash, checking deposits, and easily convertible near money) in 83% of 12-month periods. This figure significantly outpaced gold, which logged a directional alignment of 68.1%. The closest traditional asset to Bitcoin in this regard was the S&P 500 index, a benchmark for U.S. large-cap equities and a widely cited proxy for risk assets. This evidence strongly suggests that Bitcoin behaves less like an independent, uncorrelated safe haven and more like an asset whose valuation is intrinsically tied to the ebb and flow of global money supply. Randin corroborated this, noting that more recent data mirrored this pattern, with a notable rise in global liquidity during the third quarter of 2025 coinciding with Bitcoin reaching a new all-time high.

This persistent reliance on liquidity conditions highlights a fundamental challenge to Bitcoin’s "digital gold" narrative. While it may have outperformed gold over specific, short-term windows since the Iran conflict began, its deep sensitivity to liquidity means its primary reaction is to financial tightening or loosening, rather than to geopolitical stress itself. This intricate relationship complicates the straightforward idea of Bitcoin as an alternative safe haven, especially in volatile economic environments where inflation and interest rates are in constant flux.

Oil Shock Complicates Bitcoin’s Inflation Narrative

The recent Iran conflict has profoundly reshaped near-term market expectations, particularly concerning inflation. The immediate aftermath saw a dramatic surge in oil prices, driven by fears of supply disruptions following the potential closure of the Strait of Hormuz. This vital waterway, a chokepoint for a significant portion of the world’s oil supply, would have severe global economic repercussions, feeding directly into inflationary pressures.

Randin elaborated on how these rising inflation concerns, directly linked to geopolitical shocks, tend to work against Bitcoin in the short term. He explained that higher oil prices translate into elevated inflation expectations. In response to potential inflation, central banks, such as the U.S. Federal Reserve, become more hawkish, reducing the likelihood of interest rate cuts and keeping real yields (nominal interest rates minus inflation) elevated. This chain of events collectively tightens financial conditions, which in turn suppresses overall risk appetite in the market, thereby limiting demand for speculative assets like Bitcoin. In essence, Bitcoin is not reacting to inflation itself, but rather to the policy response that follows inflationary pressures.

The Iran conflict pushed Brent crude oil prices above $110 per barrel, exacerbating inflation fears. In response, the Federal Reserve, in its March 2026 summary of economic projections, raised its 2026 personal consumption expenditures (PCE) inflation forecast to 2.7% and signaled a more cautious path towards easing monetary policy. This hawkish stance by central banks reinforces the tightening of liquidity that negatively impacts Bitcoin. Interestingly, a temporary de-escalation signal, such as former President Trump’s Tuesday announcement to pause Iran strikes, had an immediate effect, pulling Brent crude oil prices back down, illustrating the direct link between geopolitical events, oil, and market sentiment.

Randin emphasized a critical distinction: “Bitcoin could be better understood as a long-term monetary debasement hedge rather than a short-term inflation hedge.” He clarified, “It responds to the expansion of money supply over multi-year cycles, not to CPI prints. On the timescale of a war-driven oil shock, it still behaves like the risk asset it is.” This perspective reframes Bitcoin’s value proposition not as an immediate shield against transient inflationary spikes, but as a long-term protector against the gradual erosion of purchasing power caused by sustained increases in the money supply.

Bitcoin Rebounds During Iran Conflict but Risk Profile Remains

Despite its recent rally, Bitcoin’s overall behavior during the Iran conflict continues to align with its classification as a risk asset. Each significant escalation in geopolitical tensions has typically triggered swift selloffs, leading to cascading liquidations and a tighter correlation with equity markets. This pattern persists even as Bitcoin has occasionally demonstrated greater resilience than traditional assets over specific, shorter periods.

Randin contextualized this performance: “But it’s important to remember the context. Bitcoin entered this conflict already in a technical bear market, down over 40% from its October highs and well ahead of equities in pricing in deteriorating conditions.” He added, “So while it has held up relatively well since the strikes began, outperforming the S&P 500, gold, and silver over certain windows, it hasn’t given us any meaningful directional move.” A true structural shift, signifying a definitive break from this established pattern and a firm establishment of its safe haven role, would require clear, sustained signals that have yet to materialize.

However, beneath the surface of price action, on-chain data presents a more nuanced picture of Bitcoin’s underlying health. Indicators such as continued accumulation by long-term holders, declining reserves on exchanges (suggesting less immediate selling pressure), and growing holdings among large wallets point to a persistent and genuine belief in Bitcoin’s long-term value proposition among a segment of investors. This strategic positioning suggests that capital is building within the Bitcoin ecosystem, even if current macro conditions are preventing this accumulation from fully translating into immediate, upward price momentum.

Nevertheless, this underlying positioning remains significantly constrained by prevailing macroeconomic conditions. Pinnock reiterated this point, explaining, “Right now, inflation driven by a hike in oil prices due to geopolitical factors is pushing yields higher and keeping central banks hawkish, which tightens liquidity. That creates a ‘bad inflation’ regime where BTC falls alongside other risk assets.” He concluded, “The inflation hedge thesis breaks because Bitcoin responds more to monetary expansion than to inflation itself, and currently, conditions are restrictive, not stimulative.”

In conclusion, while Bitcoin’s recent rally in the wake of the Iran strikes has been noteworthy, it does not definitively prove its role as a safe haven. Its performance largely appears to be a function of global liquidity dynamics and its inherent nature as a high-beta risk asset, rather than a clear decoupling from traditional markets during times of crisis. Until liquidity conditions ease significantly and Bitcoin demonstrates a consistent ability to act as a genuine counter-cyclical asset, moving independently or inversely to equities during periods of heightened stress, its claim as a true "digital gold" or safe haven asset remains, for now, unproven.