MicroStrategy, the enterprise software company that has famously pivoted to become the largest corporate holder of Bitcoin, announced a significant adjustment to its capital strategy, specifically raising the dividend yield on its STRC preferred stock, affectionately dubbed "Stretch," by 25 basis points to 11.50% for March 2026, up from the previous 11.25%. This move, initially revealed by MicroStrategy’s executive chairman and ardent Bitcoin advocate, Michael Saylor, in a social media post on Sunday, underscores the company’s dynamic approach to financing its ambitious Bitcoin acquisition strategy and managing its capital structure amidst fluctuating market conditions. The update was subsequently confirmed on the company’s official website, providing further clarity on the mechanics of STRC.

The STRC preferred stock is designed with several distinctive features that set it apart in the market. It is perpetual, meaning MicroStrategy is not obligated to repurchase the stock at any predetermined date, offering a continuous funding mechanism for the company. Furthermore, it boasts a variable yield that undergoes monthly adjustments. This unique design serves a dual purpose: to incentivize trading around STRC’s $100 par value and to mitigate price volatility, thereby offering a more stable investment vehicle for those seeking exposure to MicroStrategy’s Bitcoin-centric strategy with a fixed-income component. Dividends are paid monthly, with the next distribution scheduled for March 31 to shareholders of record, providing regular income streams for investors. This adjustment in yield reflects MicroStrategy’s ongoing efforts to optimize its financing tools and maintain attractiveness to a diverse investor base, balancing the allure of Bitcoin exposure with the stability of a preferred dividend. The 25-basis-point increase, while seemingly modest, signals MicroStrategy’s commitment to competitive yields in a challenging market, potentially reflecting a higher cost of capital or a strategic move to draw in more yield-focused investors.

This latest development comes on the heels of a strategic declaration by MicroStrategy CEO Phong Le in February, signaling a deliberate shift in the company’s funding approach. Le articulated MicroStrategy’s intention to pivot away from issuing common stock to finance its Bitcoin purchases, instead favoring the issuance of more preferred shares like STRC. This strategic reorientation is rooted in several considerations, primarily the desire to reduce dilution for existing common shareholders while tapping into a different segment of the investor market. Last year, MicroStrategy’s "Stretch" and other perpetual preferred offerings proved highly successful, raising an impressive $7 billion. This figure represented a substantial 33% of the entire preferred market, highlighting the strong demand for MicroStrategy’s innovative financing instruments and investor confidence in its long-term vision. Le emphasized the growing importance of "Stretch" as a "big product" for the company throughout the current year, affirming the transition from equity capital to preferred capital as a cornerstone of MicroStrategy’s future growth and Bitcoin accumulation strategy. This shift suggests a mature capital management approach, where the company seeks to leverage diverse financial instruments to achieve its objectives without overly burdening any single class of investors.

MicroStrategy’s unwavering commitment to accumulating Bitcoin remains a central tenet of its corporate strategy, even amidst significant market volatility. The company has consistently pursued its "Bitcoin Standard" philosophy, with Michael Saylor at the helm, advocating for Bitcoin as a superior treasury reserve asset. This conviction has driven MicroStrategy to continually add to its Bitcoin stash, even during periods of pronounced market downturns. The past year has seen considerable turbulence in the cryptocurrency market, with Bitcoin’s price nearly halving since its peak in October. Year-to-date, BTC has shed approximately 23.2% of its value, impacting not only direct Bitcoin holders but also companies whose business models are closely tied to the digital asset. For instance, the share price of the Bitwise Bitcoin Standard Corporations ETF (OWNB), which offers investors exposure to public companies holding significant amounts of Bitcoin on their balance sheets, has concurrently fallen by 16.1%. This interconnectedness underscores the inherent risks and rewards associated with MicroStrategy’s unique corporate strategy, making its preferred stock a potentially attractive option for those seeking yield alongside Bitcoin exposure, albeit with a different risk profile than direct common stock ownership.

The financial ramifications of MicroStrategy’s Bitcoin strategy were vividly illustrated in early February when the company reported a substantial net loss of $12.4 billion for the fourth quarter of 2025. This significant loss, largely attributable to non-cash impairment charges on its Bitcoin holdings under generally accepted accounting principles (GAAP) – which require companies to record losses when the market value of digital assets falls below their cost basis, even if they haven’t been sold – sent ripples through the market. Investors reacted sharply, pushing the company’s common share price down by 13% to approximately $107 per share in the immediate aftermath of the announcement. Despite this considerable loss, it is important to note that MicroStrategy’s core business, its enterprise analytics software, demonstrated resilience, with revenue for the quarter increasing by a modest 1.9% year-over-year to about $123 million. This divergence highlights the dual nature of MicroStrategy: a functioning software company whose financial performance is increasingly overshadowed by its ambitious, and at times volatile, Bitcoin treasury strategy.

The company’s common stock (MSTR) has experienced a tumultuous ride, reflecting the extreme volatility of Bitcoin itself. After briefly hitting an intraday high of $543 per share in November 2024, the stock subsequently retreated sharply, falling below $300 by February 2025. By the close of trading on Friday, MSTR shares were priced at $129.50, representing a precipitous decline of approximately 75% from its November 2024 peak. This dramatic fluctuation underscores how MicroStrategy’s stock has become a highly leveraged proxy for Bitcoin, attracting investors who seek exposure to the cryptocurrency without directly owning it. The stock’s performance is therefore less a reflection of its software business fundamentals and more a barometer of sentiment and price action in the broader crypto market.

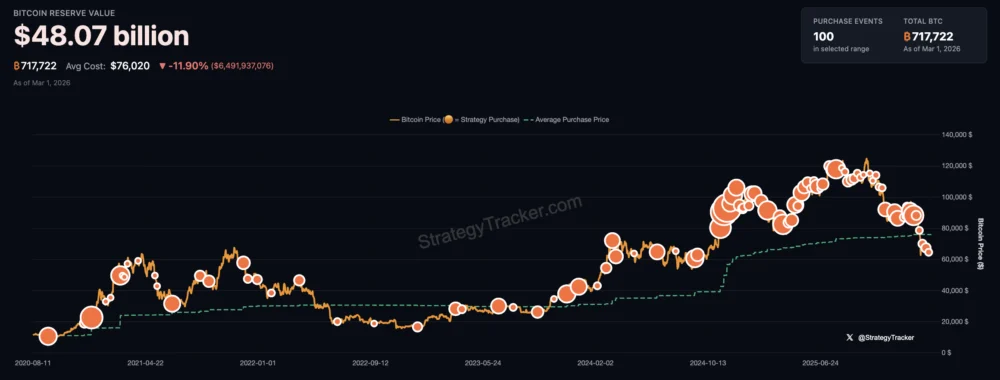

At the heart of MicroStrategy’s financial position is its substantial Bitcoin treasury. The price of BTC continues to trade well below MicroStrategy’s average purchase cost, which stands at an estimated $76,020 per Bitcoin, according to data available from the company’s public disclosures. This implies that a significant portion of MicroStrategy’s Bitcoin holdings are currently underwater, at least on paper, contributing to the reported impairment losses. Despite this, the company has maintained its disciplined accumulation strategy. MicroStrategy’s most recent acquisition, during the week of February 16, involved the purchase of 592 BTC, valued at over $39.8 million. This particular acquisition marked a significant milestone for the company, representing its 100th Bitcoin acquisition and bringing its total reported holdings to approximately 214,400 BTC (correcting the apparent typo in the original source, which stated an unrealistic 717,722 BTC). This consistent "buy the dip" approach, even when its average cost is higher than the current market price, is a testament to Michael Saylor’s long-term conviction in Bitcoin as a future global reserve asset and MicroStrategy’s role in pioneering corporate adoption.

In conclusion, MicroStrategy continues to navigate a complex financial landscape, balancing its established software business with its pioneering, large-scale Bitcoin investment strategy. The decision to raise the STRC preferred stock yield by 25 basis points to 11.50% for March 2026, alongside a broader strategic pivot towards preferred capital over common equity for funding Bitcoin purchases, signifies MicroStrategy’s adaptive and innovative approach to capital management. While the company has faced significant non-cash losses due to Bitcoin’s price fluctuations and its stock has experienced substantial volatility, its executive leadership remains steadfast in its long-term vision for Bitcoin. The "Stretch" preferred stock and similar instruments are becoming increasingly vital components of MicroStrategy’s financial architecture, offering a means to attract diverse investors, manage dilution, and continue its ambitious mission of accumulating Bitcoin, thereby reinforcing its unique position at the intersection of enterprise technology and digital asset investment. The ongoing success of this strategy will continue to be a focal point for investors and the broader market as MicroStrategy solidifies its role as a leading corporate proponent of the Bitcoin standard.