Financial institutions, recognizing the inevitable shift towards digital assets, have already committed considerable capital and resources to developing the necessary infrastructure. Major players like JPMorgan, BNY Mellon, and Citigroup have been at the forefront of this innovation. JPMorgan developed its Onyx blockchain payments network, a private blockchain platform designed to facilitate institutional-grade payments and digital asset services. BNY Mellon, a global custodian, launched comprehensive digital asset custody services, enabling institutional clients to hold and manage cryptocurrencies alongside traditional assets. Citigroup has actively tested tokenized deposits, exploring how traditional bank deposits can be represented as programmable digital tokens on a blockchain, offering enhanced efficiency and interoperability. These investments are not trivial; they encompass talent acquisition, technology development, compliance systems upgrades, and strategic partnerships, all aimed at integrating blockchain technology and digital assets into their core offerings.

However, the full realization of these strategic investments is stymied by ongoing debates in legislative and regulatory bodies regarding the classification of stablecoins. Lawmakers and regulators are grappling with whether stablecoins should be treated as traditional bank deposits, subject to existing banking laws and protections; as securities, falling under the purview of securities laws typically enforced by the Securities and Exchange Commission (SEC); or as a distinct payment instrument, requiring a new regulatory framework tailored to their unique characteristics. "Their general counsels are telling their boards that you cannot justify the capital expenditure until you know whether stablecoins will be treated as deposits, securities, or a distinct payment instrument," Butler explained to Cointelegraph. This ambiguity creates an untenable situation for banks, whose risk and compliance departments, integral to their operational integrity, cannot greenlight the full deployment and scaling of these new services without definitive legal clarity. The "infrastructure spend is real, but regulatory ambiguity caps how far those investments can scale because risk and compliance functions will not greenlight full deployment without knowing how the product will be classified," Butler argued, emphasizing the practical roadblocks faced by banks.

In stark contrast, crypto firms have historically operated, and continue to operate, with a greater degree of flexibility in these regulatory gray zones. Their business models are often built around navigating nascent legal landscapes, and they are typically structured to be more adaptable to rapid changes or the absence of clear rules. This inherent agility allows them to launch new products and services, including stablecoin-based offerings, without the same level of legal and compliance overhead that binds traditional banks. Banks, by their very nature and their fiduciary responsibilities to depositors and shareholders, "cannot operate comfortably in that gray area," Butler added. Their robust internal controls, strict adherence to Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations, and the imperative to protect consumer funds mean they must operate within clearly defined legal boundaries, or risk severe penalties and reputational damage. This dichotomy creates an uneven playing field, where innovative crypto firms can capture market share while regulated banks remain on the sidelines, awaiting legislative action.

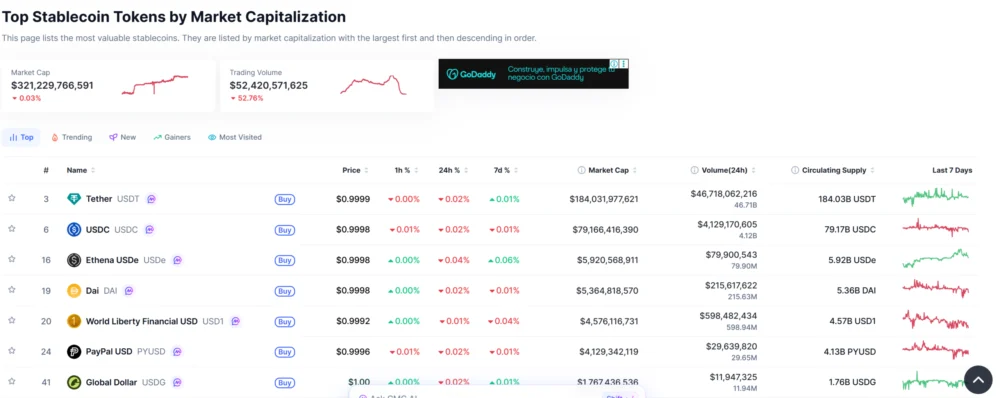

Beyond the operational paralysis, a significant concern for traditional banks is the widening "yield gap" between returns offered on stablecoin platforms and those available through conventional bank accounts. Crypto exchanges and decentralized finance (DeFi) protocols frequently offer annual percentage yields (APYs) ranging from 4% to 5% on stablecoin balances, through mechanisms like lending, staking, or liquidity provision. This stands in stark contrast to the average US savings account, which typically yields less than 0.5%, and often far less, making traditional banking a less attractive proposition for capital seeking returns.

History provides a powerful precedent for how quickly depositors can shift funds in pursuit of higher yields. Butler referenced the significant migration of funds into money market accounts during the high-interest rate environment of the 1970s. That historical precedent, however, involved a relatively slower, more cumbersome process of physical transfers and paperwork. Today, the digital nature of stablecoins and the seamless integration of crypto platforms mean that transferring funds from a traditional bank account to a stablecoin platform can take mere minutes, accelerating the potential for capital flight. The yield gap is not only significant but also easily accessible, posing an existential threat to banks’ deposit bases.

While Fabian Dori, chief investment officer at Sygnum, acknowledges the growing competitive gap, he suggests that a large-scale deposit flight is not an immediate certainty. He points to the enduring importance of factors such as trust, established regulatory oversight, and operational resilience, which continue to draw institutional clients to traditional banks. However, Dori cautions that "the asymmetry can accelerate migration at the margin, especially among corporates, fintech users, and globally active clients already comfortable moving liquidity across platforms." These segments, often more sophisticated and yield-sensitive, are likely to be the first to move. "Once stablecoins are treated as productive digital cash rather than crypto trading tools, the competitive pressure on bank deposits becomes much more visible," Dori concluded, underscoring the transformative potential of stablecoins as a fundamental payment and savings instrument.

Furthermore, Butler warned against the potential unintended consequences of attempts to restrict stablecoin yield. Under current US law, stablecoin issuers are generally prohibited from directly paying yield to holders, reflecting a regulatory desire to prevent stablecoins from circumventing traditional banking regulations. However, crypto exchanges and platforms ingeniously bypass this by offering returns through lending programs, staking mechanisms on proof-of-stake blockchains, or various promotional rewards tied to stablecoin holdings. If lawmakers were to impose broader, more stringent restrictions on these yield-generating activities, the likely outcome would not be a cessation of yield-seeking behavior, but rather a redirection of capital into less regulated, often offshore, alternative structures.

One such alternative gaining traction is synthetic dollar tokens, exemplified by products like Ethena’s USDe. These instruments generate yield not through traditional reserves or lending but through complex derivatives markets, typically employing a delta-neutral strategy involving staking Ether and shorting ETH perpetual futures. Such mechanisms can offer attractive returns even if regulated stablecoins are prevented from doing so. If this trend accelerates, regulators could inadvertently achieve the opposite of their intended outcome: rather than protecting consumers and stabilizing the financial system, they could drive more capital into opaque, less transparent offshore structures with fewer consumer protections and higher systemic risks. "Capital doesn’t stop seeking returns," Butler observed, highlighting the fundamental human economic drive that regulation must account for.

The implications of this regulatory uncertainty extend beyond individual banks and crypto firms to the broader financial system and the economy. A significant shift of deposits from traditional banks could impact their ability to lend, affecting economic growth and credit availability. It could also complicate monetary policy transmission, as central banks rely on the banking system to implement interest rate changes. From a financial stability perspective, the growth of unregulated, high-yield stablecoin platforms or synthetic dollar products could introduce new systemic risks, especially if these platforms lack robust risk management, transparency, or sufficient liquidity during times of stress.

Other global jurisdictions are moving more decisively. The European Union’s Markets in Crypto-Assets (MiCA) regulation, for instance, provides a comprehensive framework for stablecoins, categorizing them as e-money tokens or asset-referenced tokens, and imposing strict requirements on issuers regarding reserves, redemption rights, and operational resilience. Similarly, the UK, Singapore, and Hong Kong are progressing with their own frameworks. The fragmented and hesitant approach in the US risks ceding leadership in digital asset innovation and potentially driving talent and capital to more hospitable regulatory environments.

Ultimately, the call for clear and comprehensive stablecoin regulation in the US is not merely a plea from the banking sector; it is an urgent necessity for fostering innovation responsibly, protecting consumers, maintaining financial stability, and ensuring the competitiveness of the American financial system in an increasingly digitized global economy. Without a definitive stance on stablecoin classification and operational parameters, traditional banks will remain at a distinct disadvantage, potentially accelerating a paradigm shift that could fundamentally alter the landscape of finance.