At its core, Spark is driven by Phoenix Labs, a key contributor renowned for its foundational work in designing MakerDAO’s stablecoin and its intricate risk architecture. This deep expertise in decentralized stablecoin mechanics and risk management positions Spark uniquely to cater to the stringent demands of institutional clients. The new suite, as articulated by Spark, is meticulously crafted to enable professional borrowers to access stablecoin loans efficiently, bypassing the operational overhead typically associated with direct DeFi engagement. This simplification is crucial for traditional financial entities seeking exposure to digital assets while adhering to existing compliance and operational frameworks.

The newly launched Spark Prime is tailored for flexible, high-volume trading and lending activities. It introduces a sophisticated margin-style lending model coupled with off-exchange settlement capabilities, all powered by Spark’s robust liquidity engine. This combination allows for greater capital efficiency and reduced counterparty risk, features highly prized by active trading firms and hedge funds. Margin-style lending, a common practice in traditional finance, enables borrowers to leverage their capital, amplifying potential returns, while off-exchange settlement minimizes on-chain transaction costs and potential slippage, enhancing operational efficiency. Early adopters of Spark Prime include notable players such as Edge Capital, M1, and Hardcore Labs, signaling strong industry interest and confidence in Spark’s approach.

Complementing Spark Prime is Spark Institutional Lending, a dedicated offering designed to integrate Spark-governed markets directly with qualified custodians. This integration is a game-changer for institutions, allowing clients to maintain their collateral within regulated custody environments, such as those provided by Anchorage Digital. The ability to keep assets within a regulated and secure custodial framework addresses one of the primary hurdles for traditional institutions entering the DeFi space: regulatory compliance and asset security. By partnering with established custodians, Spark is effectively extending the trust and security of traditional finance into the decentralized lending landscape, paving the way for a new era of institutional DeFi adoption.

The scale of Spark’s ambition is already evident in its early traction. Sam MacPherson, co-founder and CEO of Phoenix Labs, revealed in an interview with Cointelegraph that the institutional lending arm has already secured approximately $150 million in commitments. MacPherson expressed strong confidence in the platform’s capacity, stating it has the potential "to scale to billions over the coming months." Spark Prime, while starting with a more modest $15 million in commitments, is slated for a more gradual expansion. This cautious approach is intentional, allowing Spark to progressively roll out "key safety features" designed to ensure the utmost security and stability as the platform scales. These safety features likely encompass advanced risk management protocols, enhanced collateral monitoring, and robust governance mechanisms, all critical for attracting and retaining institutional capital.

Spark’s current standing in the DeFi landscape is already substantial, reflecting its strategic partnerships and robust infrastructure. According to data from DeFi Llama, a leading analytics platform for decentralized finance, Spark’s total value locked (TVL) stands at an impressive $5.24 billion. While this figure is down from its peak of $9.2 billion in November 2025, it firmly positions Spark among the larger DeFi money market platforms by assets. To put this into perspective, Aave, a long-standing leader in DeFi lending, currently commands a TVL of $27 billion, while Maple Finance, another institutional-focused lending protocol, sits at $2.1 billion. Spark’s ability to maintain a significant TVL, even during market fluctuations, speaks to the underlying demand for its services and the trust placed in its platform.

A cornerstone of Spark’s proven capability lies in its strategic collaborations with major players in the traditional and digital financial sectors. Notably, Spark has been instrumental in powering Coinbase’s Bitcoin-backed loan market on Morpho, a decentralized lending protocol. Spark supplied more than 80% of the USDC liquidity for this initiative, contributing significantly to approximately $500 million in loan growth within the first three months of its operation. Public dashboards further corroborate this, indicating that Spark-linked vaults have deployed over $600 million to that market since its inception. This partnership not only demonstrates Spark’s capacity to handle large-scale liquidity provisions but also highlights its critical role in enabling mainstream crypto platforms like Coinbase to offer advanced financial products.

Beyond Coinbase, Spark has also extended its influence to PayPal’s foray into the stablecoin market. The PayPal USD (PYUSD) stablecoin program has leveraged approximately $500 million in Spark-governed liquidity. This collaboration has been crucial in deepening on-chain markets for PYUSD and other stablecoins, enhancing their liquidity and utility within the broader crypto ecosystem. Such high-profile partnerships with industry giants like Coinbase and PayPal underscore Spark’s growing importance as a foundational layer for institutional engagement with stablecoins and DeFi. These collaborations validate Spark’s technology and its ability to meet the rigorous demands of large-scale financial operations, solidifying its position as a trusted intermediary.

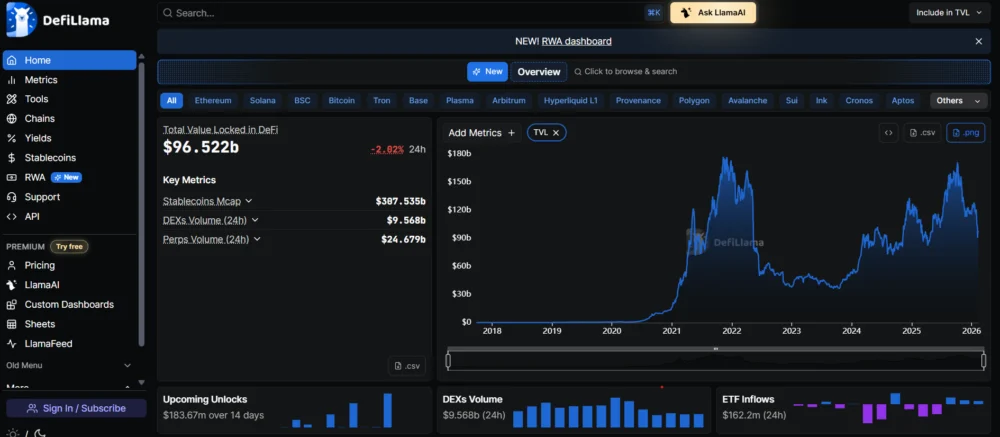

The launch of Spark’s institutional lending suite also occurs against a fascinating backdrop of the DeFi market’s resilience. While the broader cryptocurrency market has experienced significant volatility and a notable selloff, DeFi has demonstrated a relative robustness. The overall DeFi TVL, currently at $96.52 billion, has seen a decline from around $120 billion at the end of January. This represents approximately a 20% decrease during the recent crypto market downturn. In contrast, major cryptocurrencies have experienced steeper declines over the same period. Bitcoin (BTC), for instance, dropped from about $89,000 at the end of January to approximately $66,800 at the time of writing, a decline of about 25%. Ether (ETH) saw an even more pronounced fall, from roughly $3,000 to around $1,950, representing a decrease of approximately 35%, according to data from Coingecko.

This comparative resilience of DeFi suggests a maturing market where utility-driven protocols, particularly those focused on stablecoin lending and borrowing, are proving to be more stable than speculative assets. This trend aligns with the insights of industry thought leaders like Vitalik Buterin, who has drawn a distinction between "real DeFi" and centralized yield stablecoins, emphasizing the importance of genuinely decentralized and transparent protocols. Spark’s model, with its emphasis on transparency and on-chain verifiability, aligns well with the principles of "real DeFi."

MacPherson further elaborated on a critical advantage of Spark’s model: its inherent transparency. He argued that "anyone can evaluate the full portfolio in real time," a feature that is transformative for institutional participants. This unprecedented level of transparency allows institutions to rigorously underwrite Spark’s books against their own internal limits and risk tolerance frameworks. Crucially, it also empowers them to exit positions promptly "if the profile does not align with their risk controls." This ability to continuously monitor and assess risk in real-time is a significant departure from the often opaque practices of traditional finance, offering institutions a level of control and insight that is rarely available in conventional markets. Such transparency fosters trust and enables institutions to integrate DeFi lending into their existing risk management strategies with greater confidence.

The journey of DeFi from a niche, experimental technology to a sophisticated financial ecosystem capable of attracting institutional capital is marked by innovations like Spark’s new lending suite. By addressing the critical needs of institutions – regulatory compliance through qualified custodians, enhanced security, operational efficiency, and transparent risk management – Spark is actively lowering the barriers to entry for traditional finance. The ability to channel vast reserves of DeFi stablecoins into institutional credit markets represents a significant evolution, potentially unlocking trillions of dollars in liquidity and fostering a more interconnected global financial system. As Spark continues to scale its operations and roll out advanced safety features, its impact on the convergence of decentralized and traditional finance is poised to be profound, redefining how institutions interact with digital assets and stablecoin-powered lending.