Florida lawmakers have decisively approved a pioneering state-level framework designed to regulate payment stablecoins, a significant move that now places the landmark legislation on Governor Ron DeSantis’ desk for final approval, signaling Florida’s intent to lead in the evolving digital asset landscape. This comprehensive bill, known as Senate Bill 314 (SB 314), received unanimous support from the Florida Senate, echoing its earlier passage in the House. The bipartisan consensus underscores a shared vision within the state’s legislature to foster innovation while simultaneously implementing robust consumer protection and financial oversight mechanisms for this crucial segment of the cryptocurrency market.

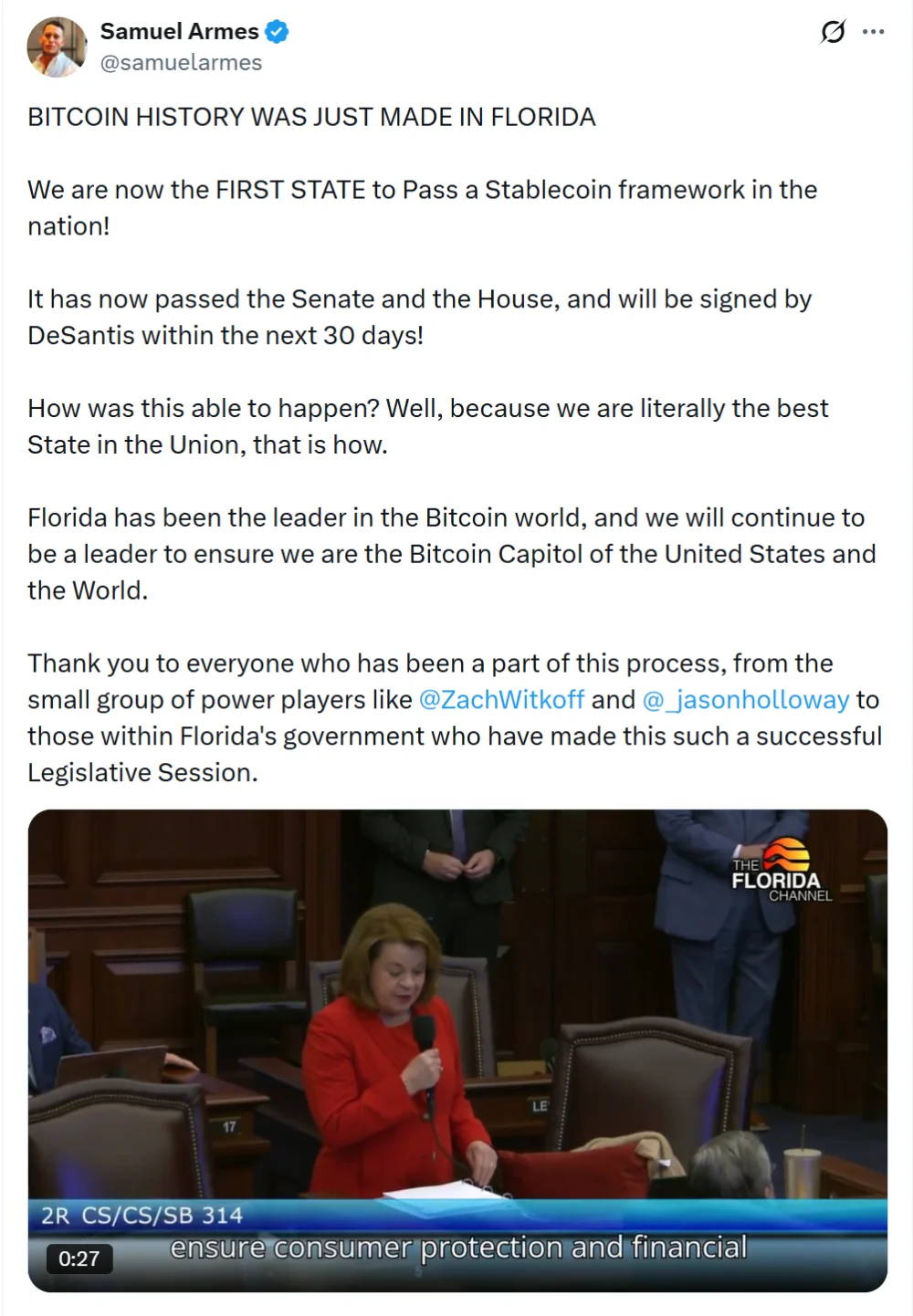

The imminent enactment of SB 314 was heralded by Samuel Armes, the founder of the Florida Blockchain Business Association, who, in a recent post on X, confirmed the bill’s successful clearance through both chambers. Armes expressed optimism that Governor DeSantis would sign the measure into law within the next 30 days, solidifying Florida’s position as a forward-thinking jurisdiction in digital finance. His enthusiastic declaration, "It has now passed the Senate and the House, and will be signed by DeSantis within the next 30 days!" encapsulates the anticipation within the state’s burgeoning blockchain community. This legislative action positions Florida as one of the first states to establish a dedicated regulatory framework for stablecoins, setting a potential precedent for other states grappling with how to integrate digital assets into their existing financial systems.

At its core, SB 314 establishes clear regulatory guidelines for entities involved in issuing payment stablecoins within Florida’s jurisdiction. This proactive approach aims to provide much-needed clarity for businesses and consumers alike, addressing the current patchwork of regulations that often characterizes the broader crypto space. Working in tandem with House Bill 175, the legislation introduces a suite of consumer protection standards and financial oversight rules that are meticulously aligned with the federal GENIUS Act, a pivotal piece of legislation signed into law in July. The alignment with federal efforts highlights Florida’s commitment to creating a harmonized regulatory environment, rather than a conflicting one, thus reducing potential friction for businesses operating across state lines and at a national level. The GENIUS Act itself focuses on ensuring that stablecoins maintain their pegged value and are backed by adequate reserves, providing a blueprint for state-level adaptations like Florida’s.

One of the most critical aspects of SB 314 is its explicit amendment to Florida’s Control of Money Laundering in Money Services Business Act. This update is not merely an administrative tweak; it signifies a fundamental recognition of stablecoins as legitimate, albeit regulated, financial instruments. By explicitly including stablecoins within the ambit of existing anti-money laundering (AML) and counter-terrorist financing (CFT) regulations, the state is ensuring that stablecoin issuers are held to the same stringent standards as traditional financial institutions. This amendment mandates that all stablecoin issuers comply with established financial regulations, a crucial step in mitigating illicit activities often associated with unregulated digital assets. Furthermore, the bill unequivocally bans the unlicensed issuance of stablecoins within the state, underscoring Florida’s commitment to a regulated and transparent digital economy. This move is designed to weed out bad actors and instill greater confidence in the stablecoin ecosystem for both businesses and consumers.

Beyond addressing money laundering concerns, the legislation also provides much-anticipated clarity on the classification of stablecoins. A persistent debate in the crypto world revolves around whether stablecoins should be treated as securities, a designation that carries significant regulatory burdens under federal law. SB 314 clarifies that certain payment stablecoins will not be classified as securities, a distinction that is vital for the operational viability and growth of the stablecoin market. This legal distinction helps prevent payment-focused stablecoins, which are primarily designed for transactional utility rather than investment, from being inadvertently subjected to securities laws that are ill-suited to their function. This clarity reduces regulatory uncertainty, potentially attracting more legitimate stablecoin projects and businesses to Florida.

The bill also lays out a structured framework for the oversight of stablecoin issuers, depending on their operational base and structure. Issuers based outside Florida, for instance, will be required to notify the state’s Office of Financial Regulation (OFR) before commencing operations within the state. This provision ensures that even entities headquartered elsewhere are brought under Florida’s regulatory purview when serving its residents. The oversight mechanism itself is tiered: some stablecoin operators will fall exclusively under the jurisdiction of the OFR, a state agency responsible for the regulation of financial services, while others will face joint supervision alongside the Office of the Comptroller of the Currency (OCC). This joint supervision model is particularly relevant for stablecoins issued by federally chartered banks or other entities that already fall under federal banking oversight, fostering cooperation between state and federal regulators to avoid redundant or conflicting requirements. This nuanced approach acknowledges the diverse operational models within the stablecoin industry.

A forward-looking aspect of the law addresses potential risks associated with stablecoin incentives, particularly concerning yield or interest payments. The legislation explicitly bars qualified issuers from paying interest or yield to stablecoin holders if federal rules prohibit such payments. This clause is a pre-emptive measure to prevent stablecoins from morphing into unregistered securities through interest-bearing mechanisms, a practice that has drawn scrutiny from federal regulators like the Securities and Exchange Commission (SEC) in the past. The intent here is to maintain the fundamental characteristic of stablecoins as payment instruments rather than investment vehicles that could circumvent traditional securities regulations. By aligning with potential federal prohibitions, Florida further ensures its framework is harmonized with broader national financial stability objectives.

Florida’s progressive stance on stablecoin regulation is part of a broader, concerted effort by the state to embrace digital assets and position itself as a leader in the blockchain and cryptocurrency space. This is evident in other legislative initiatives, such as the renewed push for a state crypto investment bill. In October of the previous year, Florida lawmakers reignited efforts to integrate cryptocurrencies into state investment strategies with the filing of Florida House Bill 183 (HB 183). Filed by Republican Representative Webster Barnaby, this ambitious proposal seeks to allow the state and various public entities to allocate up to 10% of their substantial funds into a diverse portfolio of digital assets.

Notably, HB 183 represents a significant expansion from earlier proposals, moving beyond just Bitcoin (BTC) to include a wider array of crypto assets. The revised proposal now encompasses crypto exchange-traded products (ETPs), crypto securities, non-fungible tokens (NFTs), and other blockchain-based assets. This broader scope reflects an understanding of the rapidly diversifying digital asset market and a desire to capture potential benefits across different segments. The rationale behind such a move is multifaceted: it includes potential portfolio diversification, hedging against inflation, and positioning Florida at the forefront of financial innovation. By investing in these assets, the state aims to capitalize on the growth of the digital economy and potentially secure higher returns for its public funds, while also signaling its commitment to supporting the underlying technology.

HB 183 is a refined iteration of HB 487, a previous bill that was withdrawn in June after failing to advance through a House operations subcommittee. The withdrawal of HB 487 highlighted some initial hesitations and challenges in gaining full legislative consensus on state crypto investments. However, the reintroduction of the concept with an expanded scope in HB 183 demonstrates the enduring interest and determination of Florida lawmakers to pursue this strategy. The changes in the new bill likely reflect lessons learned from the previous attempt, addressing concerns by offering a more comprehensive and perhaps more appealing investment strategy. The inclusion of a wider range of assets could also mitigate some of the volatility risks associated with a Bitcoin-only approach, making it a more palatable option for risk-averse public fund managers.

The approval of SB 314, coupled with the ongoing efforts surrounding HB 183, paints a clear picture of Florida’s strategic vision for the digital economy. The state is actively working to create a welcoming yet regulated environment for cryptocurrency businesses and investors. This dual approach—regulating stablecoins for stability and consumer protection, while also exploring direct state investments in digital assets—underscores a balanced strategy aimed at harnessing the transformative potential of blockchain technology. Florida’s proactive legislative agenda could serve as a blueprint for other states, demonstrating how to navigate the complexities of digital asset regulation and integration into traditional financial systems.

However, the implementation of such a comprehensive framework will not be without its challenges. The Office of Financial Regulation will need to rapidly develop expertise and resources to effectively oversee a nascent and rapidly evolving industry. Educating businesses on new compliance requirements, attracting skilled personnel, and adapting to future technological advancements in stablecoins will be critical. Furthermore, while Florida is aligning with federal efforts, the dynamic nature of federal cryptocurrency regulation means that state laws may need continuous review and adjustment to maintain harmony and effectiveness. The final signature from Governor DeSantis, while highly anticipated, remains a crucial step in solidifying Florida’s leadership in this space.

In conclusion, Florida’s Senate approval of the first stablecoin bill marks a monumental step in the state’s journey to becoming a national leader in digital finance. By establishing a robust regulatory framework for payment stablecoins, amending anti-money laundering laws, clarifying security classifications, and setting clear oversight mechanisms, Florida is proactively fostering innovation while safeguarding consumers and maintaining financial integrity. This legislative achievement, alongside the continued pursuit of state crypto investment strategies, firmly positions Florida at the vanguard of the digital asset revolution. As Governor DeSantis prepares to sign this pivotal bill, the Sunshine State is poised to illuminate a path forward for responsible and innovative engagement with the future of money.