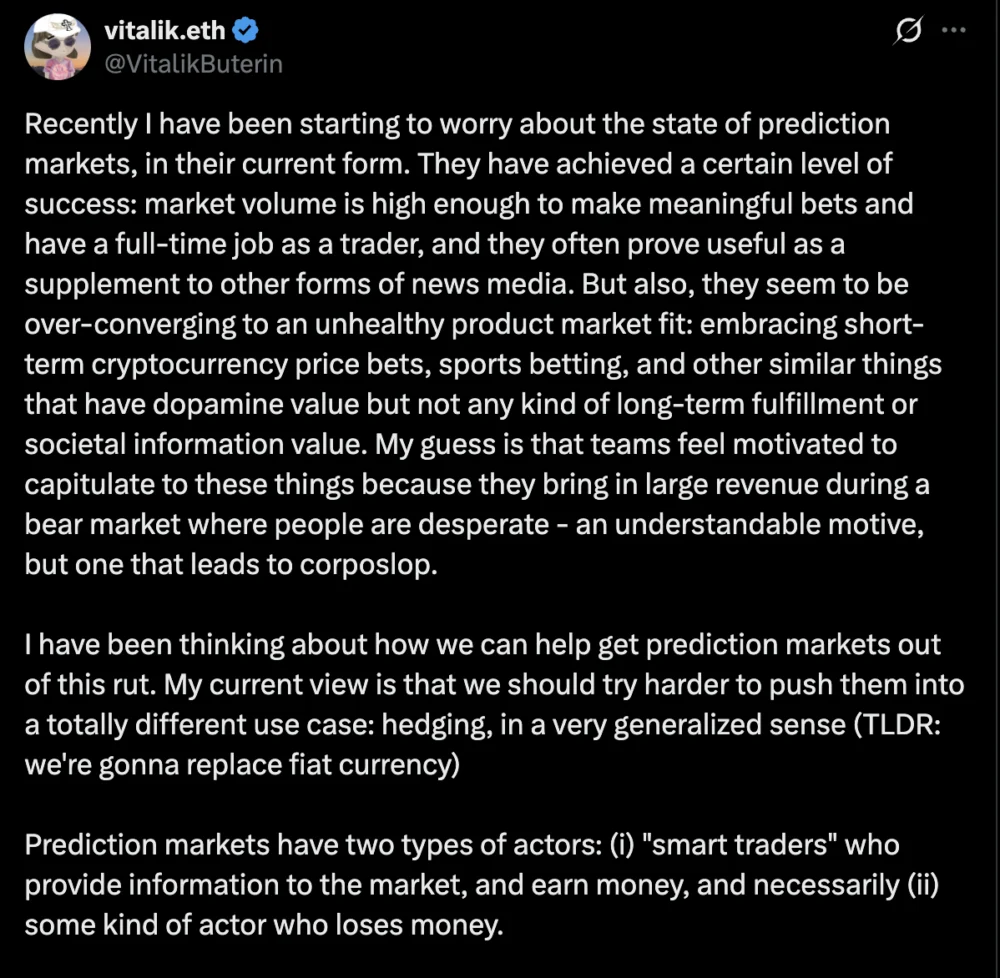

In a detailed post on X (formerly Twitter), Buterin outlined his vision, emphasizing that the intrinsic power of on-chain prediction markets, when synergistically combined with the capabilities of advanced Artificial Intelligence (AI) large-language models (LLMs), could unlock their true potential as general hedging mechanisms. This strategic pivot, he argued, would empower consumers with a novel means to achieve price stability across a broad spectrum of goods and services, effectively shielding them from the erosive effects of inflation and market fluctuations.

Buterin elaborated on the practical implementation of such a system. He envisioned the creation of comprehensive price indices encompassing all major categories of goods and services that consumers regularly purchase. These indices would be granular, segmenting physical goods and services by different geographical regions to reflect localized economic realities. For each of these meticulously defined categories, a corresponding prediction market would be established. The core innovation, however, lies in the personalized application of these markets. According to Buterin, each user, whether an individual consumer or a business entity, would be equipped with a local LLM. This AI, tailored to the user, would possess the capability to meticulously understand and analyze that user’s specific spending patterns and future expense projections. Based on this personalized financial profile, the LLM would then recommend and offer a bespoke "basket" of prediction market shares. These shares would be strategically configured to represent and hedge against the expected future expenses of that user over a specified period, for instance, ‘N’ days.

The overarching goal of this system, Buterin concluded, is to empower individuals and businesses to construct a diversified financial portfolio. This portfolio would ideally comprise a combination of traditional assets aimed at wealth accumulation and growth, alongside these "personalized prediction market shares." The latter component would serve as a dynamic financial shield, specifically designed to offset the escalating cost of living, particularly in an environment characterized by persistent fiat currency inflation. This dual approach aims to provide both upward mobility through asset growth and downward protection against the erosion of purchasing power.

Buterin’s proposal arrives amidst a broader debate about the utility and regulation of prediction markets. Supporters of these platforms frequently highlight their inherent value as powerful crowdsourced intelligence tools. They argue that prediction markets offer unparalleled insights into global events, political outcomes, and financial market trends by aggregating the collective wisdom of participants. Beyond mere forecasting, proponents also emphasize their potential to serve as flexible mechanisms for individuals and businesses to hedge against a diverse array of risks, ranging from commodity price volatility to geopolitical uncertainties.

Harry Crane, a statistics professor at Rutgers University, is a vocal advocate for prediction markets, asserting that they often demonstrate greater accuracy than traditional polls and surveys. Crane posits that these markets should be recognized and treated as a public good, providing an unfiltered and decentralized source of information. He has suggested that opposition to prediction markets, particularly from certain factions within the U.S. government, stems from their capacity to generate insights that are difficult to ignore or manipulate by centralized authorities. Platforms like Polymarket and Kalshi, Crane argues, offer a crucial alternative to information disseminated through official channels or mainstream media, which can sometimes be subject to control or manipulation to shape particular narratives or distort public opinion.

The concept of hedging, central to Buterin’s vision, involves taking an offsetting position in a related asset to reduce the risk of adverse price movements. Traditionally, hedging instruments include futures contracts, options, and various forms of insurance. Buterin’s proposal envisions prediction markets functioning as a more granular and potentially more accessible form of hedging. Instead of just hedging against broad market indices or commodity prices, consumers could hedge against the price of their specific grocery basket, their local rent increases, or the cost of their utility bills. This level of specificity, facilitated by AI-driven personalization, represents a significant departure from traditional financial instruments.

The integration of AI LLMs is critical to Buterin’s proposed system. These models would not only analyze individual spending data but also likely process vast amounts of external economic data, market sentiment, and even news events to generate accurate price predictions for the various indices. The LLM would act as a sophisticated financial advisor, dynamically adjusting the recommended basket of prediction market shares based on evolving personal finances and broader economic conditions. This personalized, dynamic hedging strategy is a key differentiator from existing static hedging solutions.

However, the implementation of such a system presents numerous challenges. Technical hurdles include ensuring the scalability and efficiency of on-chain prediction markets to handle potentially millions of personalized contracts. The accuracy and reliability of the AI LLMs in predicting localized price movements and managing sensitive personal financial data are paramount. The "oracle problem"—reliably feeding real-world price data into decentralized, on-chain markets—would need robust and decentralized solutions to prevent manipulation. Furthermore, liquidity in these highly specialized and personalized markets would be crucial; without sufficient participants willing to take the opposite side of a hedge, the markets might not function effectively.

Economically, incentivizing participation for both hedgers and liquidity providers is a complex balancing act. While consumers would benefit from price stability, the mechanisms for market makers to profit from providing liquidity and taking on risk would need to be clearly defined and attractive. Regulatory bodies worldwide are still grappling with how to classify and regulate existing prediction markets, often viewing them as gambling rather than financial instruments. A shift towards consumer hedging would necessitate a fundamental re-evaluation of these regulatory frameworks, potentially requiring new legal definitions and oversight mechanisms.

Ethical considerations also loom large. The use of local LLMs that deeply understand a user’s expenses raises questions about data privacy and security, even if the models are designed to operate locally. While Buterin suggests local LLMs, the potential for data aggregation and misuse, or even bias in the AI’s recommendations, would need careful consideration and robust safeguards. The possibility of market manipulation, even in decentralized systems, cannot be entirely discounted, necessitating strong governance and auditing mechanisms.

Despite these challenges, Buterin’s vision offers a compelling glimpse into a future where decentralized finance and AI could converge to offer tangible benefits to everyday consumers. It represents a move away from the often-criticized speculative nature of much of the crypto industry towards applications that address real-world economic problems like inflation and financial instability. If successful, such a system could democratize access to sophisticated financial hedging tools, which have historically been the preserve of large institutions and wealthy individuals.

This proposed transformation of prediction markets underscores a broader maturation within the Web3 ecosystem. The initial phase, characterized by rapid innovation and often volatile speculation, is gradually giving way to a focus on building sustainable, utility-driven applications that can integrate with and improve traditional financial systems. Buterin’s call is not just for a change in application but for a fundamental reorientation of purpose for prediction markets, positioning them as essential financial infrastructure for a more stable and equitable economic future. It challenges developers, policymakers, and users alike to consider how these powerful tools can be harnessed to serve the collective good, rather than being confined to the realm of high-stakes betting. The conversation sparked by Buterin’s insights is a vital one, pushing the boundaries of how decentralized technologies can empower individuals against the backdrop of an ever-changing global economy.