A significant legal challenge for cryptocurrency exchange Coinbase has intensified as a Delaware judge has permitted a shareholder lawsuit, alleging insider trading against several of its directors, including CEO Brian Armstrong and board member Marc Andreessen, to proceed. This pivotal decision, issued by Delaware Chancery Court Judge Kathaleen St. J. McCormick, comes despite an extensive internal investigation that had previously cleared the executives of any wrongdoing, effectively setting the stage for a potentially protracted legal battle over the company’s 2021 direct listing.

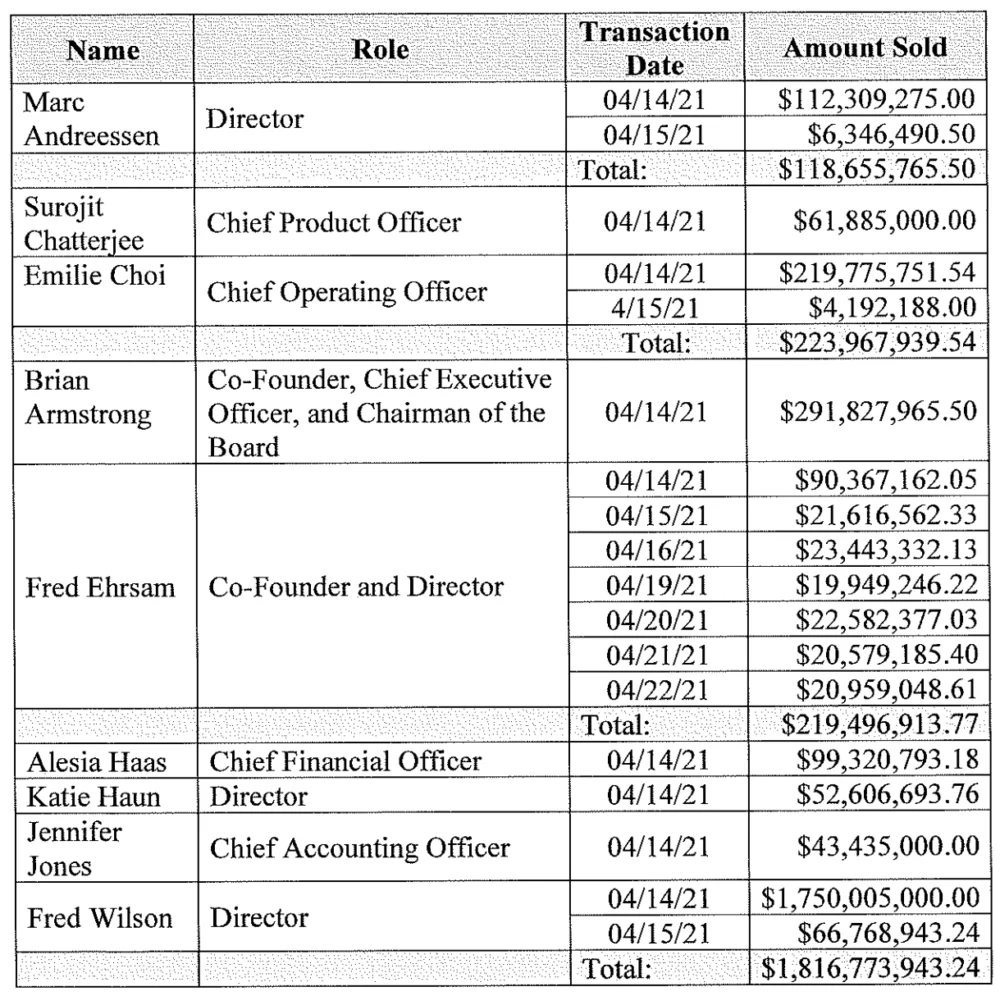

The lawsuit, originally filed in 2023 by a Coinbase shareholder, centers on serious allegations that key company directors leveraged confidential, non-public information to avert substantial financial losses, estimated to exceed $1 billion, by strategically selling their shares around the time of Coinbase’s highly anticipated public debut in April 2021. The core of the complaint posits that these insiders, possessing superior knowledge regarding the company’s true valuation and market prospects, collectively offloaded a staggering cumulative total of over $2.9 billion worth of stock. Among the named individuals, CEO Brian Armstrong is specifically accused of personally divesting approximately $291.8 million in shares. Marc Andreessen, a prominent venture capitalist and a member of Coinbase’s board since 2020, is alleged to have sold roughly $118.7 million in shares through his influential venture firm, Andreessen Horowitz (a16z). The plaintiff contends that these sales were executed under the premise that the directors were aware Coinbase’s valuation was inflated at the time of its direct listing, enabling them to circumvent subsequent declines in stock value.

Judge McCormick’s crucial ruling on Friday denied a request to dismiss the suit, which had been put forward following a comprehensive, 10-month probe conducted by a Special Litigation Committee (SLC) formed by Coinbase’s board. The SLC’s primary mandate was to independently investigate the shareholder’s allegations and recommend whether the lawsuit should continue. As reported by Bloomberg Law, the committee ultimately concluded that the claims lacked merit and recommended terminating the case. Their findings suggested that the share sales were limited in scope and primarily intended to provide necessary liquidity for the direct listing process. Furthermore, the committee argued that Coinbase’s share price movements closely mirrored those of Bitcoin (BTC) during the period in question, thus undermining the assertion that the trades were predicated on illicit insider knowledge rather than broader market dynamics.

However, Judge McCormick, while acknowledging that the committee’s findings presented a "strong defense" for the accused directors, ultimately ruled that "questions surrounding the independence of one committee member were enough to keep the case alive," per the report. The shareholder plaintiff had specifically challenged the SLC’s independence, highlighting past business relationships between committee member Gokul Rajaram and Andreessen’s firm. These connections, according to the judge, raised "legitimate concerns," even though she noted there was "no suggestion of bad faith" on Rajaram’s part. The integrity and perceived independence of such internal investigative bodies are paramount in shareholder derivative suits, particularly within the jurisdiction of the Delaware Chancery Court, which specializes in corporate law and governance. The court often scrutinizes these committees to ensure they truly act in the best interest of the company and its shareholders, free from undue influence by the very executives they are investigating.

Coinbase’s decision to go public through a direct listing in April 2021, rather than a traditional Initial Public Offering (IPO), forms a crucial backdrop to these allegations. A direct listing, unlike an IPO, allows existing shareholders to sell their shares immediately on the open market without the typical lockup period that often restricts sales for a certain duration post-IPO. Critically, direct listings also do not involve the issuance of new shares, which can dilute existing ownership. While direct listings offer advantages like avoiding underwriting fees and providing immediate liquidity for early investors, they also mean that there isn’t the same price discovery mechanism or built-in demand generation that an investment bank typically provides in an IPO. At the time of Coinbase’s listing, the cryptocurrency market was experiencing a significant bull run, with Bitcoin and other digital assets reaching new all-time highs, fueling immense excitement and contributing to a lofty valuation for the exchange. The lawsuit’s central claim is that the directors exploited the immediate liquidity provided by the direct listing, knowing that the company’s valuation was unsustainable or set to decline shortly after the public debut.

Coinbase and the named defendants have consistently and vehemently denied all allegations. The company has maintained there is no evidence whatsoever that its executives possessed or acted upon material nonpublic information when conducting their share sales. A spokesperson for Coinbase reportedly conveyed to Bloomberg Law the company’s "disappointment by the court’s decision" and reiterated its firm resolve to continue fighting what it describes as "meritless claims." This robust defense underscores the high stakes involved, not only for the individual executives but also for Coinbase’s corporate reputation and governance standards. The Delaware Chancery Court is renowned for its expertise in corporate law, making its rulings particularly influential in matters of corporate governance and fiduciary duties.

The legal journey for this lawsuit has already seen pauses and significant deliberation. The case was put on hold last year to allow the SLC to conduct its thorough 10-month review. The committee’s detailed report, which found no basis for the claims of insider trading, was intended to serve as a decisive factor for dismissal. However, Judge McCormick’s ruling highlights the stringent requirements for independence in such corporate governance mechanisms. The perceived conflict of interest, even if not indicative of bad faith, was sufficient to prevent the dismissal of the suit, thereby allowing the shareholder to continue pursuing the derivative claims on behalf of Coinbase. A shareholder derivative lawsuit is a legal action brought by a shareholder on behalf of the corporation itself, seeking to recover damages for harm done to the corporation by its directors or officers. If successful, any damages awarded would typically go to the company, not directly to the individual shareholder plaintiff, as the goal is to benefit the company as a whole. The continuation of this lawsuit means that the defendants will likely face a discovery phase, including depositions and the exchange of evidence, and potentially a trial, which can be costly and time-consuming for all parties involved.

Compounding the legal pressures, Coinbase is concurrently grappling with entirely separate allegations of insider trading, albeit involving different circumstances and a more recent timeline. Recent reports from crypto researchers have suggested that certain traders might have capitalized on advance knowledge of token listings on the Coinbase platform. These claims posit that sophisticated analysis of blockchain data and technical signals could have allowed some market participants to anticipate which digital assets the exchange was preparing to list, enabling them to trade ahead of public announcements and profit from the subsequent price surges that often accompany such listings. In response to these distinct, newer allegations, Coinbase has publicly committed to reviewing and adjusting its token listing process over the coming quarters. The company aims to implement changes designed to mitigate information leaks and reduce uneven access to market signals, demonstrating a proactive stance to uphold market integrity across its operations. This dual front of insider trading allegations – one historic concerning its direct listing and executive stock sales, and one more recent concerning token listings – underscores the ongoing scrutiny faced by major cryptocurrency exchanges regarding transparency and fairness in their trading environments.

The path ahead for the lawsuit against Armstrong, Andreessen, and other directors remains complex and uncertain. The judge’s decision ensures that the allegations will be examined further, potentially through a robust discovery phase and beyond. This case will undoubtedly continue to be closely watched by investors, corporate governance experts, and the broader cryptocurrency industry, as it touches upon fundamental questions of executive accountability, shareholder rights, and the integrity of public market debuts in the rapidly evolving digital asset space.